Assessment of oil and gas

companies’ climate strategy

6 of the largest publicly listed integrated oil and gas companies in Europe and the United States accounted for a huge 12% of near-term expansion plans, and 10% of global production in 2024.

These companies bear a major responsibility for the climate change that is already affecting entire economies and millions of people. Winding down their fossil fuel activities—including rapidly halting expansion strategies and gradually dismantling existing facilities—directly determines our ability to limit global warming to as close to 1.5°C as possible.

But is such a transformation possible, or is it just an illusion, given that most have recently backtracked on their climate commitments, announcing an increase in hydrocarbon production by 2030 and a decline in their investments in renewables?

To enable financial actors to adapt their financing, investment, and engagement strategies, Reclaim Finance has analyzed their orientations in detail. Several key indicators have been selected to assess the credibility of their climate action. All aim to answer three questions:

- What are the company’s investment choices?

- What are its production and greenhouse gas emission targets?

- To what extent is the company really diversifying?

Read about the main conclusions of our analysis and download a detailed briefing specific to each of the 12 oil and gas companies below. For your convenience, a glossary is available here.

methodology

Given the importance of cutting greenhouse gas emissions within the current decade, our analysis focuses on corporate targets for 2030.

The International Energy Agency’s (IEA) Net Zero Emissions by 2050 Scenario (NZE), which is based on a 1.5°C trajectory, was chosen as the main reference scenario. This scenario models:

- A drop in oil and gas production of 15% and 10% respectively by 2030, compared with 2024 levels.

- A halt to the development of new oil and gas fields

- A 3-fold increase in installed renewables capacity by 2030, which requires doubling current investment levels in renewable power, grids and battery storage to USD $2 to 3 trillion by 2030.

- A 60% reduction in investment in fossil fuel production between 2024 and 2035, as well as a 2.5-fold increase in “clean energy” investment over the same period to maintain reliable energy supplies.

Our analysis puts the 6 oil and gas companies’ projections into perspective against the NZE.

key findings

None of the climate strategies are aligned with a 1.5°C scenario.

Analysis of the climate strategies of these 6 oil and gas companies in relation to the NZE scenario shows that their investments, production plans and diversification strategies do not enable them to follow a 1.5°C trajectory.

Priority to shareholders and fossil fuels, particularly gas

Companies favored distributions to shareholders and investments in fossil fuels in 2025 rather than investing in sustainable energy.

Continued expansion of oil and gas

None has committed to halting oil and gas expansion, contrary to the NZE scenario and UN recommendations.

A fossil-fuel centered energy mix in 2030

All of them forecast an energy mix in 2030 that would still include between 83% and more than 99% fossil fuels.

Exceeding the 1.5°C carbon budget in 2030

All of them will emit more greenhouse gases in 2030 than allowed in a 1.5°C scenario.

Misleading diversification

Climate backtracking

Most companies backtracked on their climate commitments recently, prioritizing upstream and/or reducing support to renewable energy.

Climate strategies analysis

BP’s investment strategy

The British company reset its investment strategy in 2025, announcing a new plan that heavily relies on upstream oil and gas.

- Over the past 3 years, BP invested US$1.5 billion annually in oil and gas exploration.

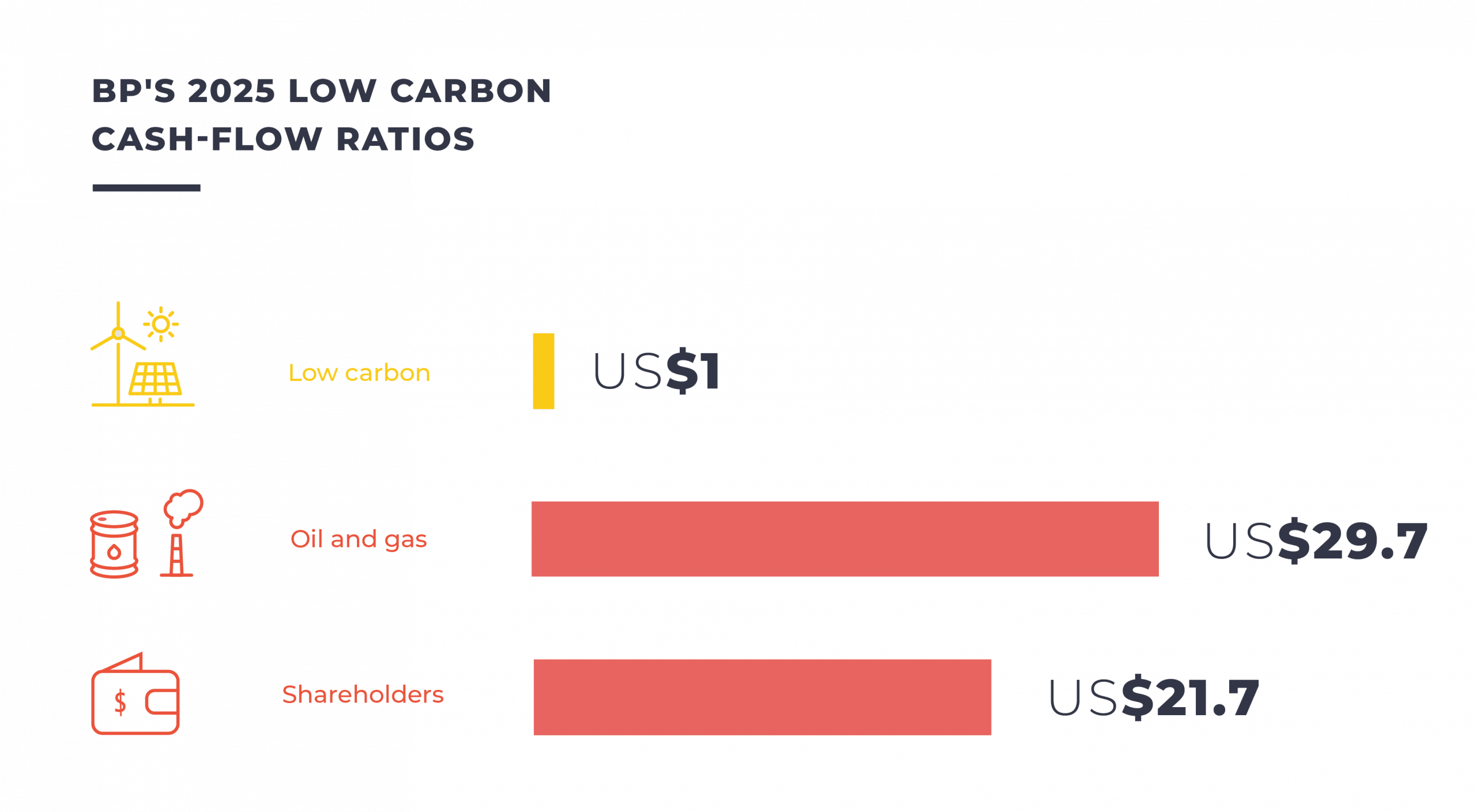

- In 2024, US$13.8 billion was invested by BP in oil production and integrated gas, and US$10.1 billion was distributed to shareholders, compared with just US$464 million invested in its “low carbon energy” business – that includes renewable energies as well as biofuels, hydrogen and carbon capture and storage.

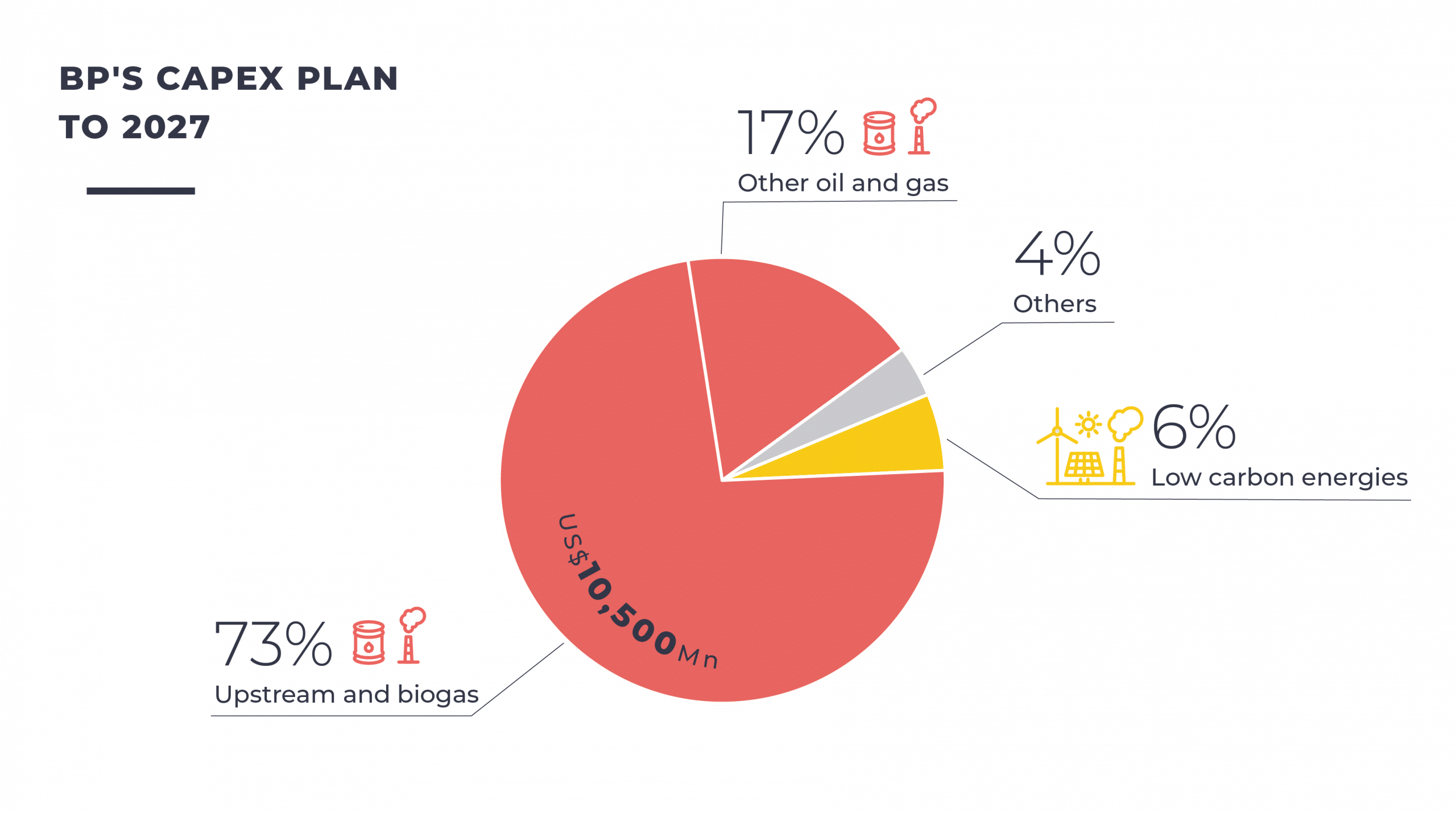

- From 2025 to 2027, BP plans to invest US$10.5 billion per year in oil and gas, and only US$800 million in “low carbon energy”. This is a significant rollback compared to the previous capital expenditure plan, which projected investing US$4 billion per year to 2030 in its “low carbon energy” business.

BP’s fossil fuel production plan

BP has not made any commitment to stop developing new oil and gas projects. The company is the 20th largest upstream developer worldwide.

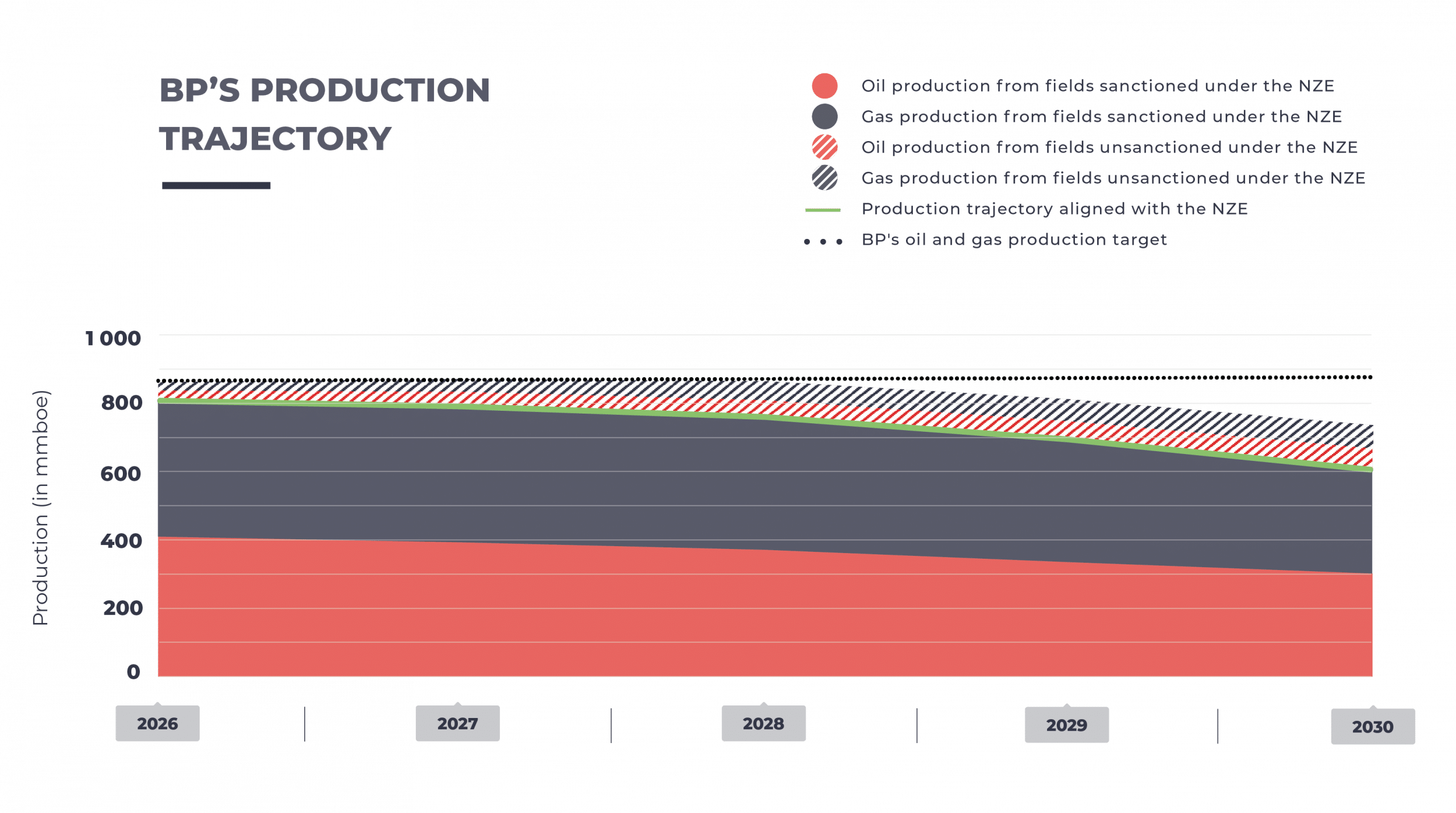

In 2023, BP rolled back on its 2030 oil and gas production reduction target. With its new strategy, the company intensified its climate backtrack, planning to slightly increase its oil and gas production by 2030 to 2.3 to 2.5 million barrels of oil equivalent per day. If it meets this target, the company production will be 57% above the level required by the NZE.

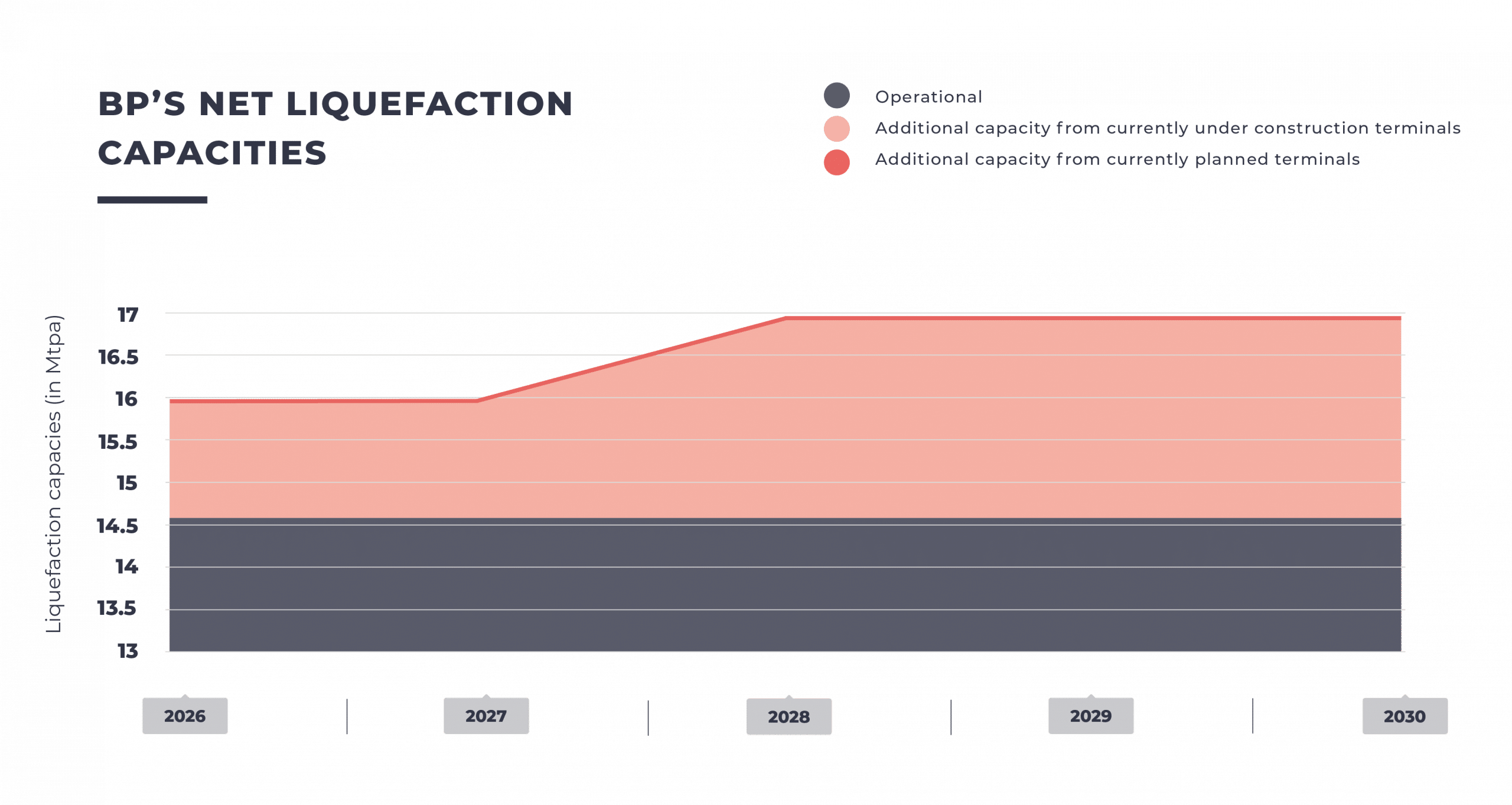

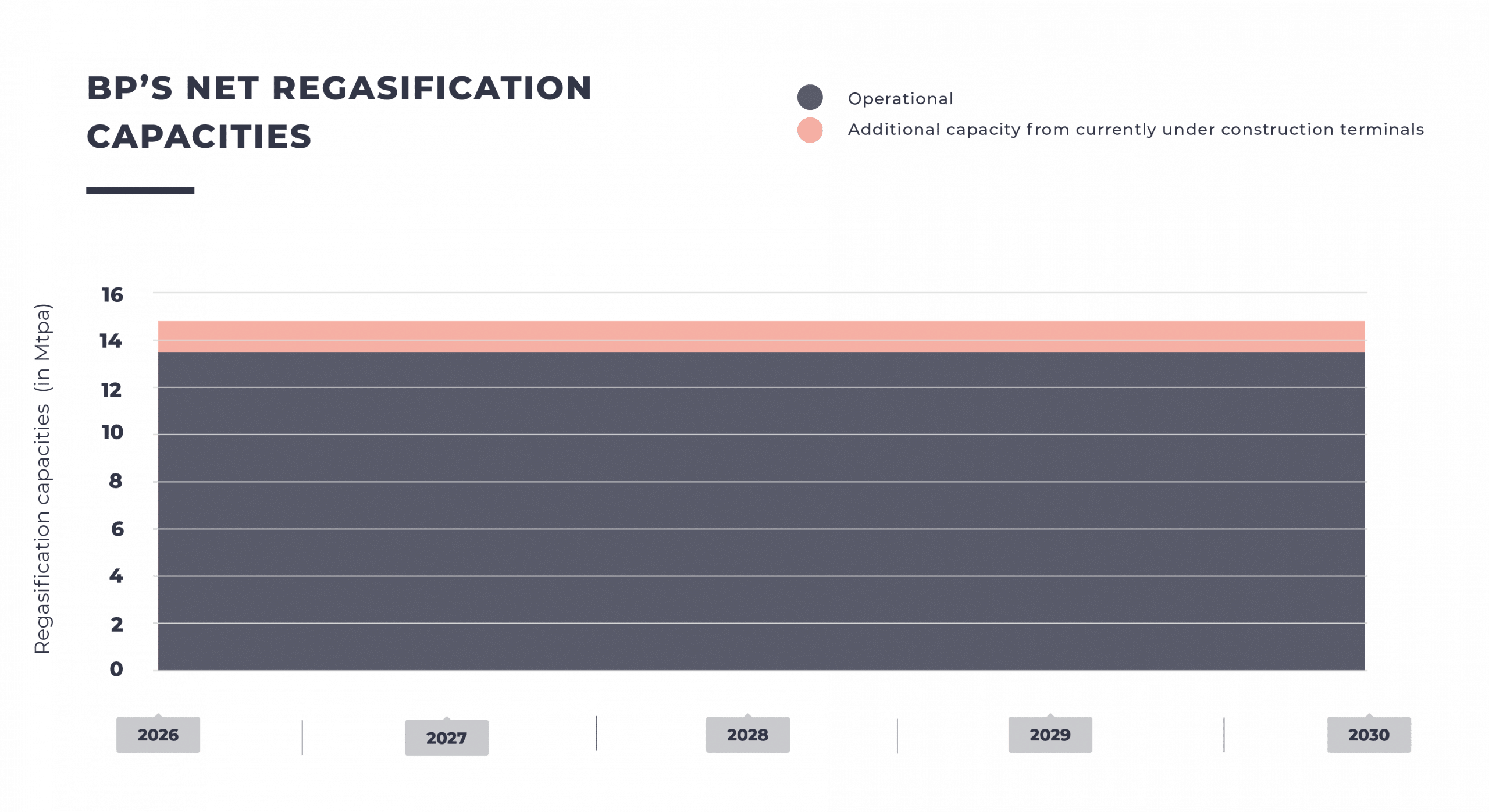

BP’s oil and gas production in 2030 will represent 1.9% of that projected globally in the NZE.LNG is part of BP’s fossil expansion strategy with new export and import terminals under construction. BP’s net liquefaction capacity will increase to 16 Mtpa by 2030 and will overshoot by 16.2% the level previously required by the NZE.

BP’s diversification strategy

The company’s business model will continue to be based on oil and gas extraction and LNG in the coming years. Diversification into other energies will continue to represent a minority share of BP’s future production and will sometimes involve activities that are harmful to the environment. As of today, BP also specifies that, within the low-carbon category, a large part of the investments will be directed towards hydrogen and CCS.

A central part of BP’s electricity generation expansion strategy relies on gas power. BP has 1.6 GW of net gas power capacity planned through four new gas plant units – one of them being in Europe.

BP does not communicate a target on its future renewable capacities beyond 2025 anymore. The development of renewable energy has significantly dropped in the new strategy with a focus on capital light partnerships rather than organic development of new renewable infrastructures.

Eni’s investment strategy

The Italian company’s investment strategy heavily relies on hydrocarbons, in particular on upstream and midstream gas.

- Between 2023 and 2025, Eni invested an average US$1.3 billion per year in oil and gas exploration.

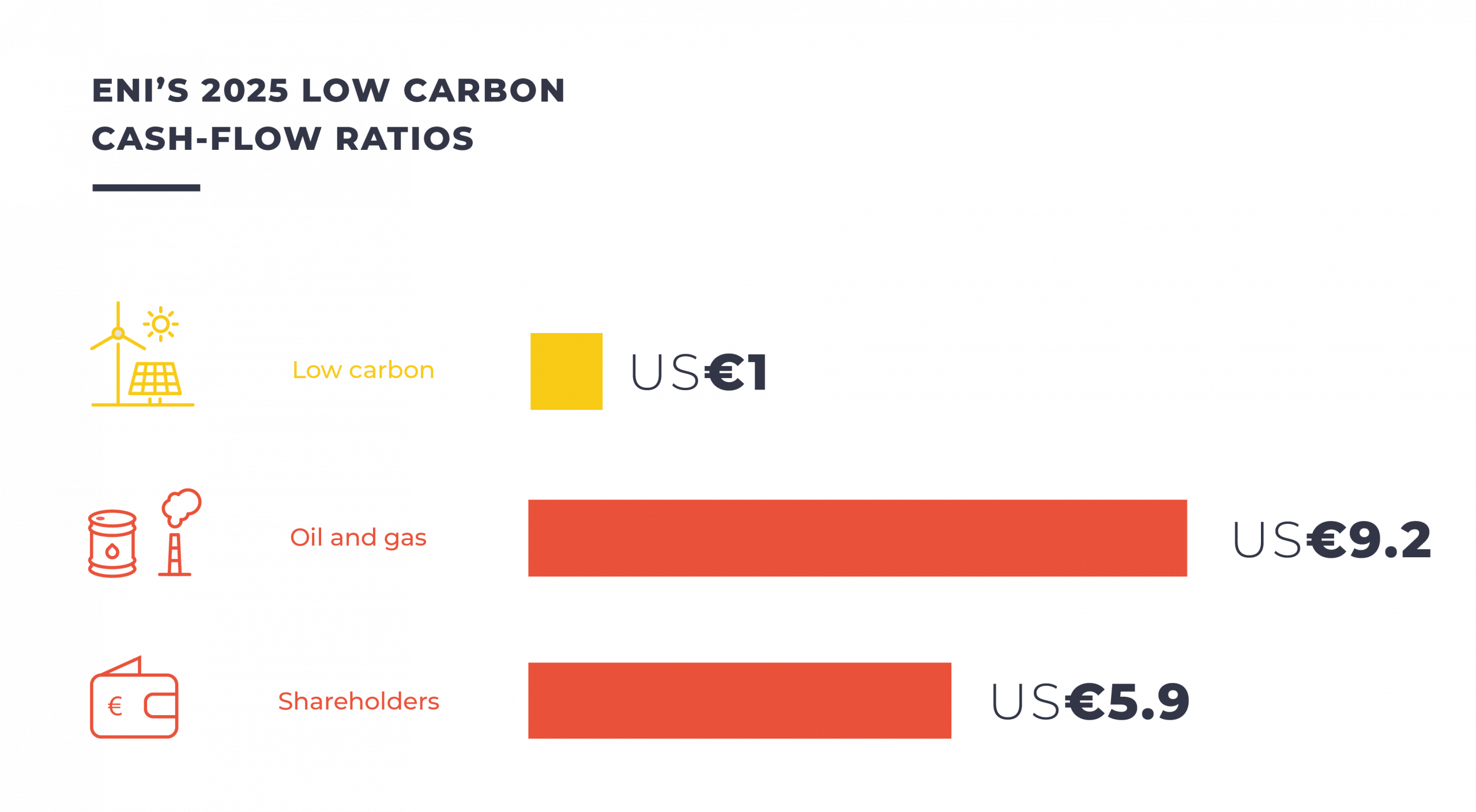

- In 2024, €6.9 billion were invested in oil and gas – primarily upstream – and €4.5 billion were distributed to shareholders, compared with only €764 million invested in Plenitude – that includes renewable electricity, other so-called “low carbon” energies, as well as gas distribution.

- Through 2030, Eni plans to allocate at least 57% of its investments to oil and gas. 35% of its investments (including Plenitude’s own expenditures, as a demerger of Eni and Plenitude is ongoing) will be allocated to low carbon energy, which in this case also includes gas distribution. The rest, approximately 8%, goes to other activities including Enilive’s refining of fossil-based and bio fuels.

Eni’s fossil fuel production plan

Eni has made no commitment to stop developing new oil and gas projects. The company is the 13th largest upstream developer worldwide and the 23rd largest LNG export terminal developer.

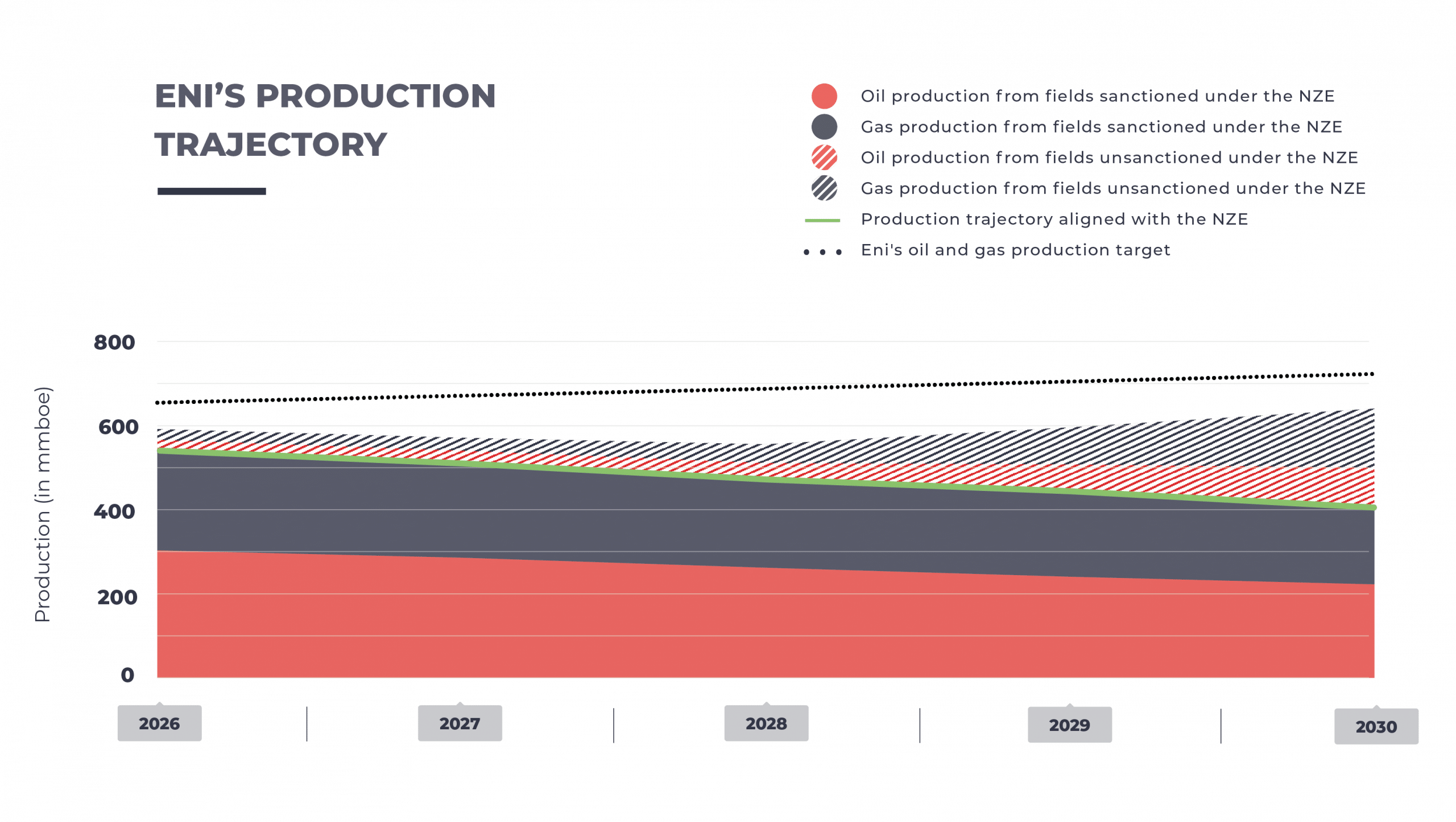

Eni has continuously increased its reported oil and gas production target over the past years. The company now plans to increase its oil and gas production by 3-4% per year through 2030 instead of 2-3% per year as previously targeted. With the company’s current expansion strategy, its 2030 fossil fuels production will be 78% above the NZE.

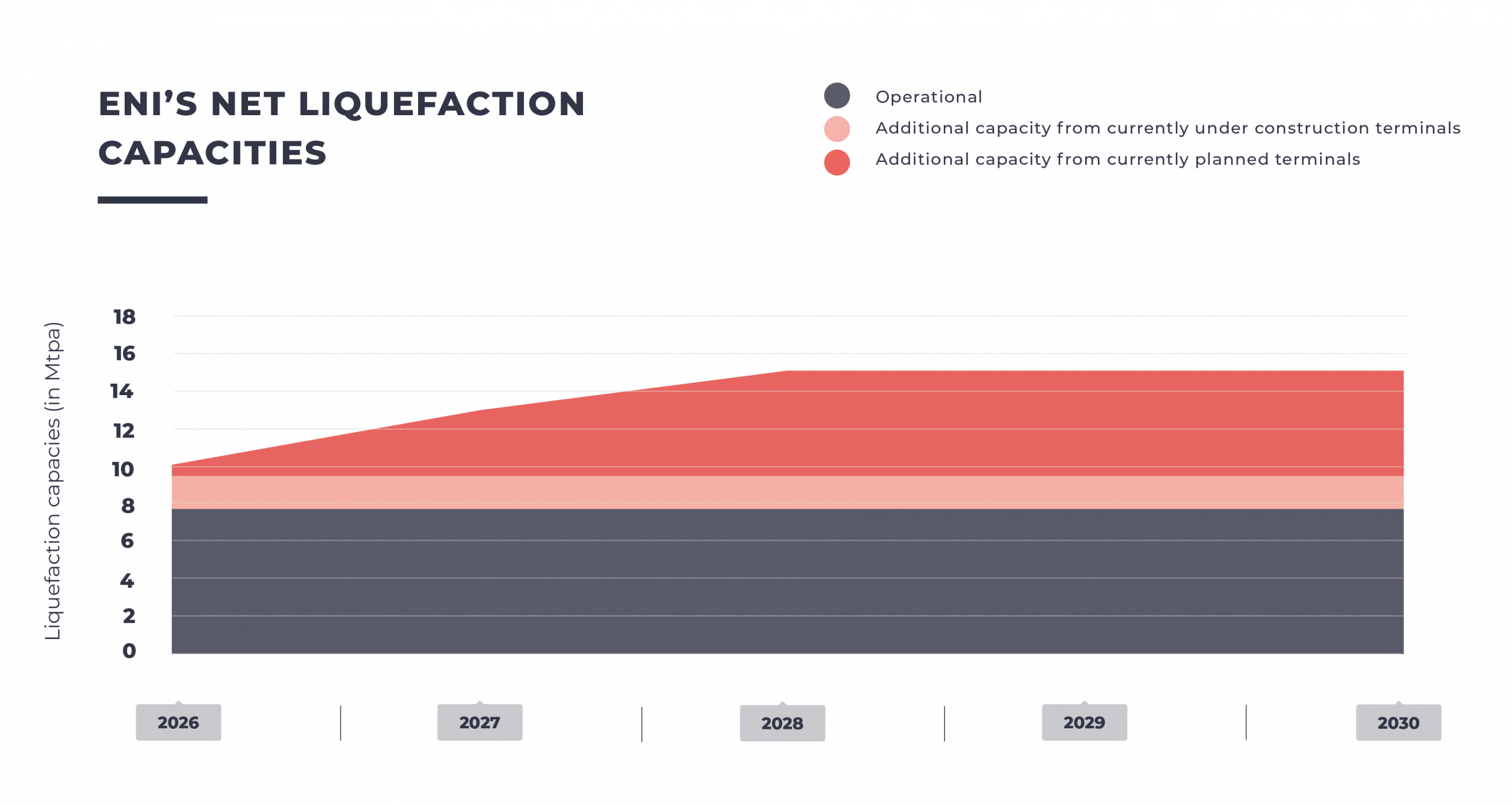

LNG is core to Eni’s gas-oriented expansion strategy with new export terminals planned. Eni’s net liquefaction capacity will increase to 15 Mtpa by 2030 and will overshoot by 96% the level previously required by the NZE.

Eni’s diversification strategy

The company’s business model will continue to be based on oil and gas extraction and LNG in the coming years. Diversification in other energies will keep representing a minority share of its future production and will sometimes involve activities that are harmful to the environment.

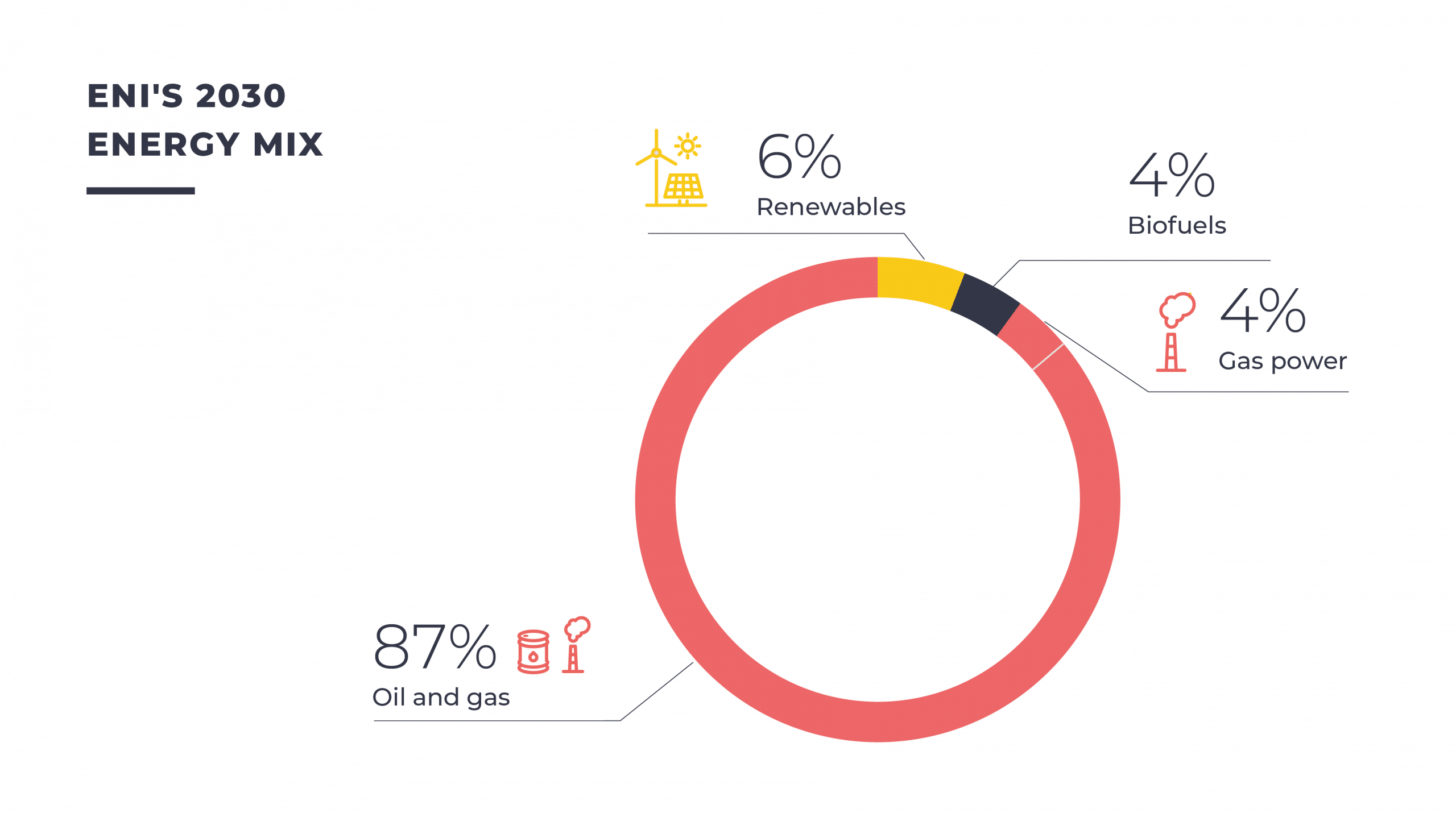

Eni’s power strategy heavily relies on gas power, 81% of its electricity being fossil-based as of 2024. Eni is planning six new gas power units, that will represent a 12% increase of its gross gas power capacity.

In 2026, the Italian major sticks to its installed renewable capacity target of 15 GW in 2030 (similar to that announced in 2025). Renewable power will then represent 6% of Eni’s production mix.

With its current strategy, Eni will remain one of the key oil and gas players. Indeed, in 2030, Eni’s oil and gas extraction will represent 1.5% of the global hydrocarbon production projected in the NZE, whereas the company will only represent 0.1% of the worldwide renewable power production.

Equinor’s investment strategy

The Norwegian company’s investment strategy increasingly prioritizes the oil and gas sector and redistribution to shareholders.

- Over the past 3 years, Equinor has invested US$1.2 billion annually in oil and gas exploration.

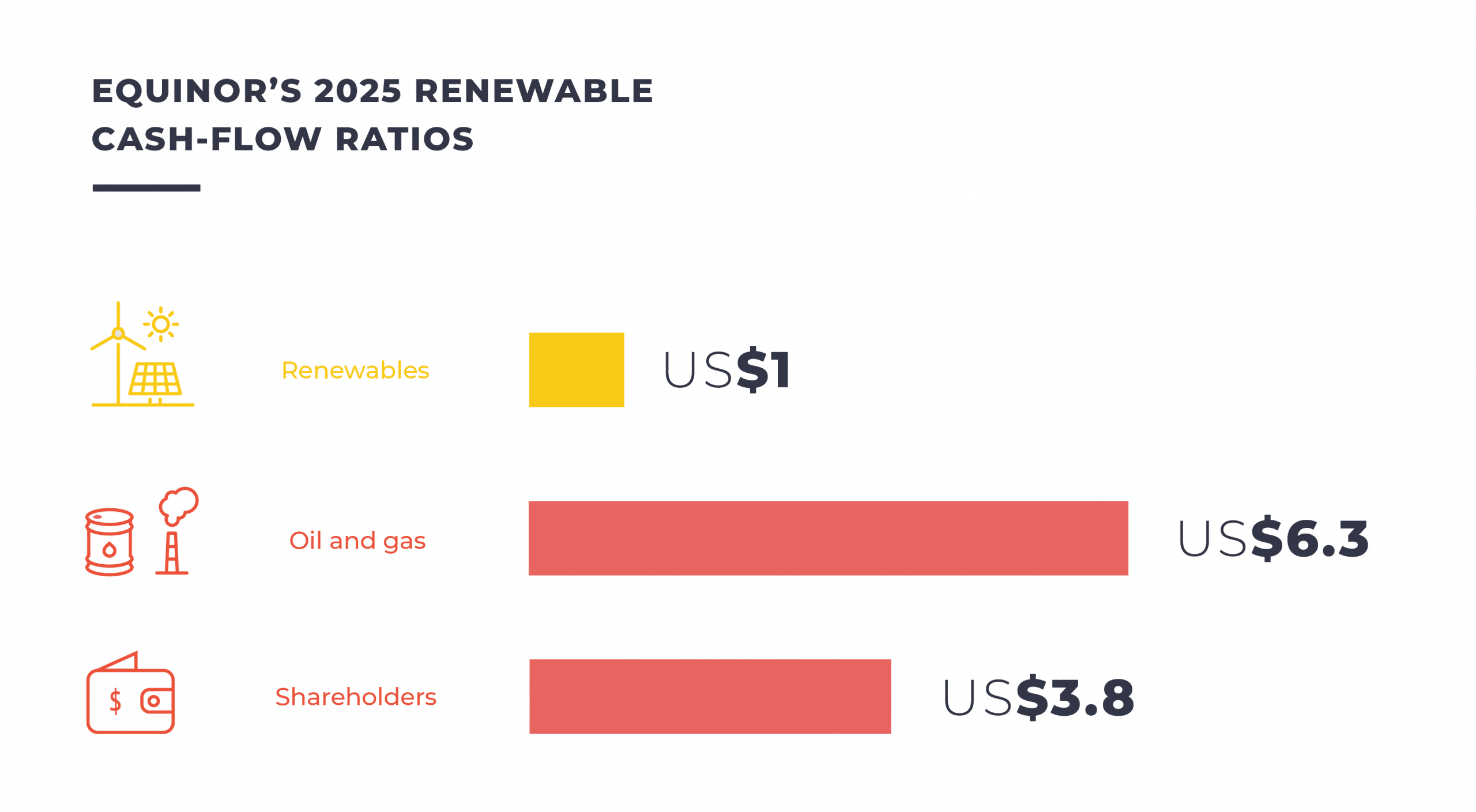

- In 2025, US$16.8 billion were invested by the company in oil and gas exploration and production, and US$10.7 billion were distributed to shareholders, compared with US$2.8 billion invested in renewables.

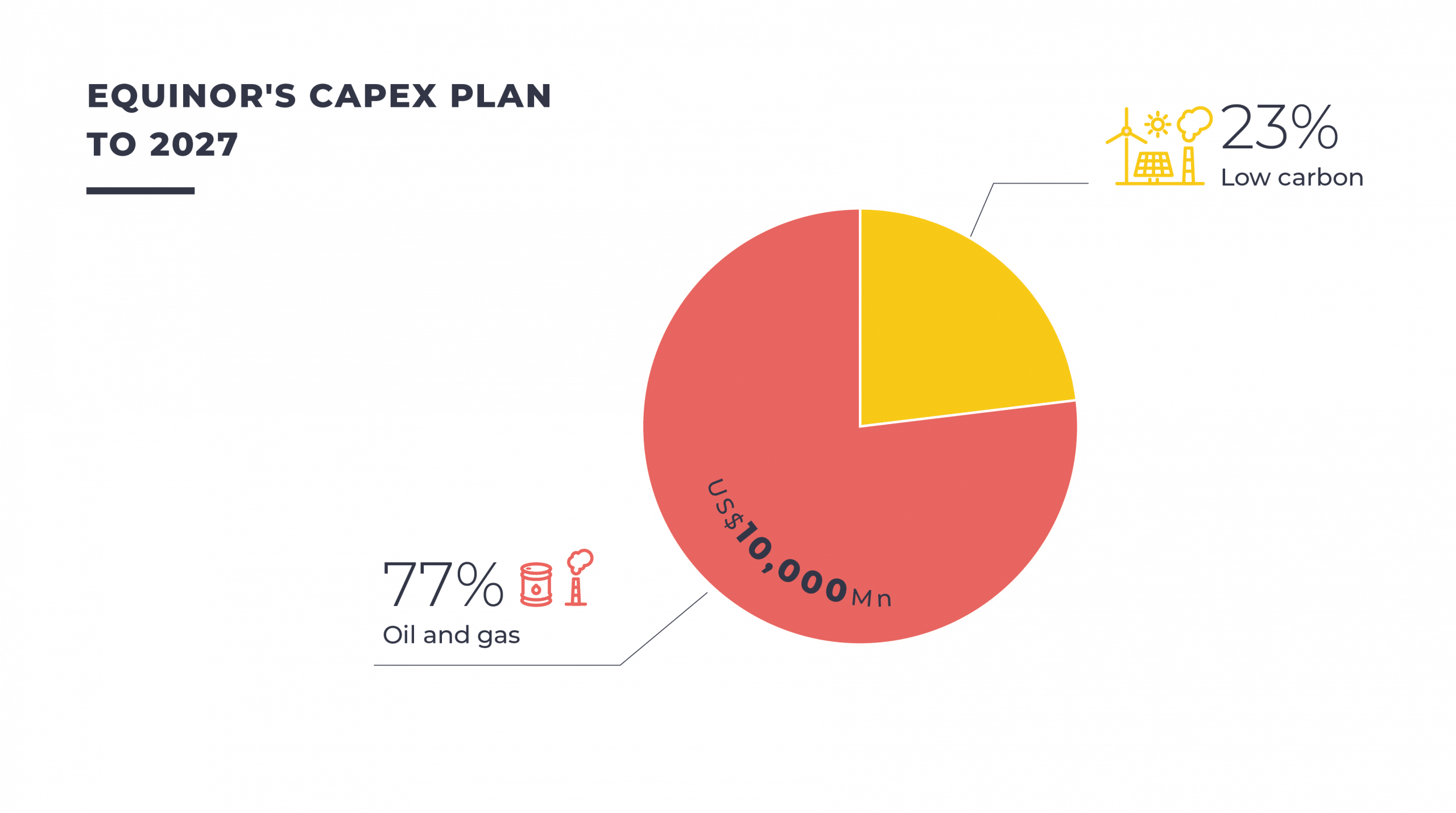

- Through 2027, Equinor now plans to allocate approximately 23% of its investments to renewables and ”low carbon” activities, way below the announced 38% in 2025. The 2025 provision was already a significant rollback compared to the previous plan, which targeted to allocate 50% of its gross investments in “low carbon” activities by 2030.

Equinor’s fossil fuel production plan

Equinor has made no commitment to stop developing new oil and gas projects. The company is the 22nd largest upstream developer worldwide and the 42nd largest LNG export terminal developer.

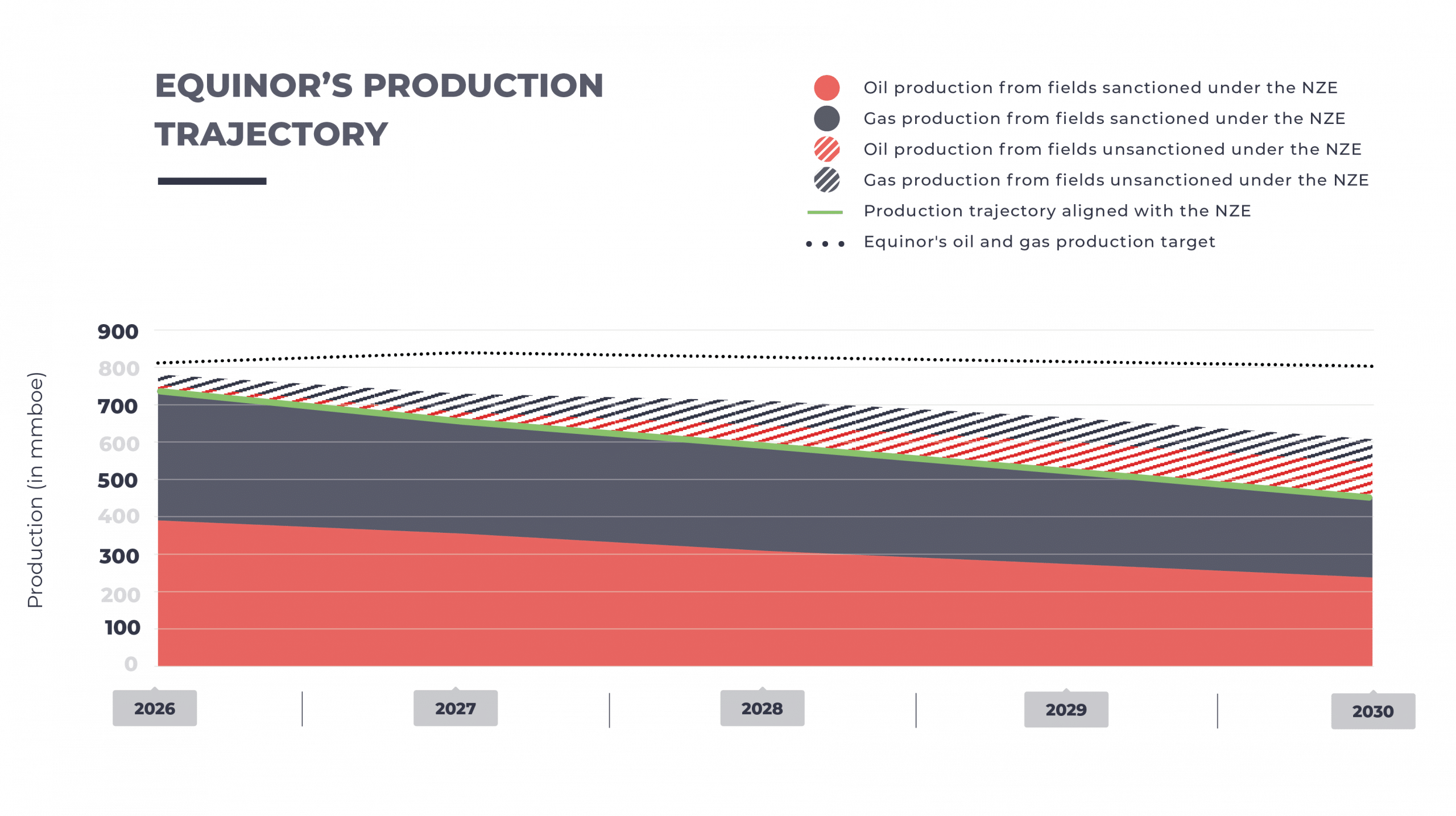

In 2025, Equinor changed its commitment to reduce its oil and gas production to 2 million barrels of oil equivalent per day by 2030,replacing it by a 2.2 million objective, 10% higher than previously targeted. This is slightly above Equinor’s 2025 production level, meaning that the company does not plan to decrease its production anymore. With the company’s current expansion strategy, its 2030 fossil fuels production will be 80% above the NZE.

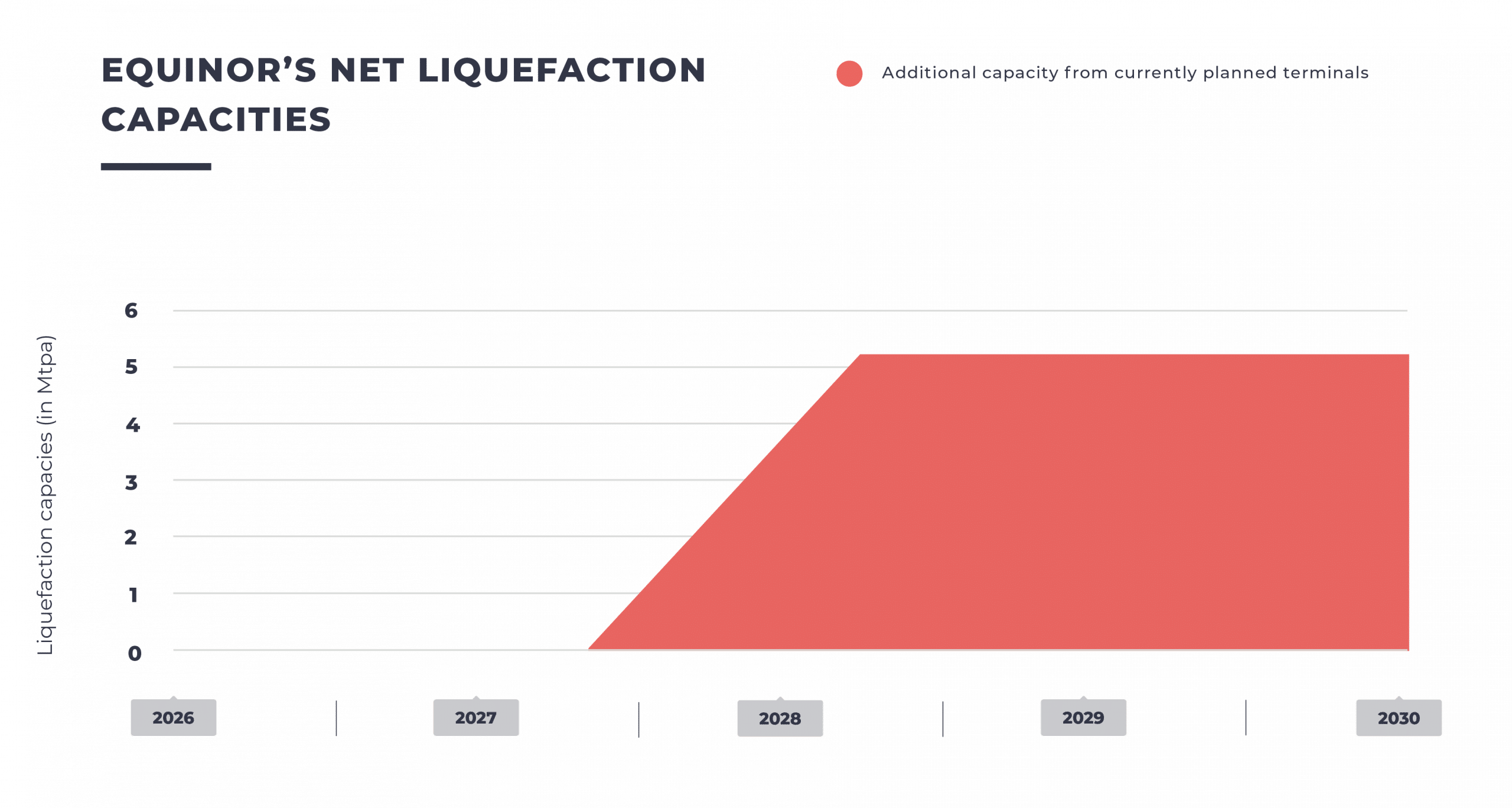

LNG is a major component of Equinor’s gas-oriented expansion strategy. While the company does not own any export terminal yet, it plans to develop one new export terminal before 2030. Equinor’s net liquefaction capacity will then increase to 5.2 Mtpa by 2030, then overshooting the 2024 NZE.

Equinor’s diversification strategy

The company’s business model will be based on oil and gas extraction and LNG in the coming years. Diversification in other energies will keep representing a minority share of its future production and will sometimes involve activities that are harmful to the environment. Equinor’s electricity strategy vastly relies on gas power. Equinor is planning a new gas power unit that will represent a 50% increase in Equinor’s gross gas power capacity.

In 2025, Equinor dropped its commitment to reach 12 to 16 GW of installed capacity by 2030 and abandoned its 2030 net renewable generation target. Now, Equinor is only targeting 10 to 12 GW of installed or under development net capacity and has not set any updated renewable production target. Assuming Equinor will meet its targets, its energy production from renewables will be 20.9 times lower than its energy production from oil and gas in 2030.

With its current strategy, Equinor will remain one of the key oil and gas players. Indeed, in 2030, Equinor’s oil and gas extraction will represent 1.6% of the global hydrocarbon production projected in the NZE, whereas the company will only represent 0.1% of the worldwide renewable power production.

Shell’s investment strategy

The British – Dutch company’s investment strategy heavily relies on hydrocarbons, in particular on upstream and integrated gas:

- Over the past 3 years, US$2.2 billion per year were invested by Shell in oil and gas exploration.

- In 2024, US$14.0 billion were invested in upstream and integrated gas – that primarily includes LNG activities – and US$22.5 billion were distributed to shareholders, compared with just US$1.9 billion invested in its “Renewables and Energy Solutions” business – that includes renewable energy and other so-called “low carbon” energies. This is down compared to the US$2.5 billion invested in 2024.

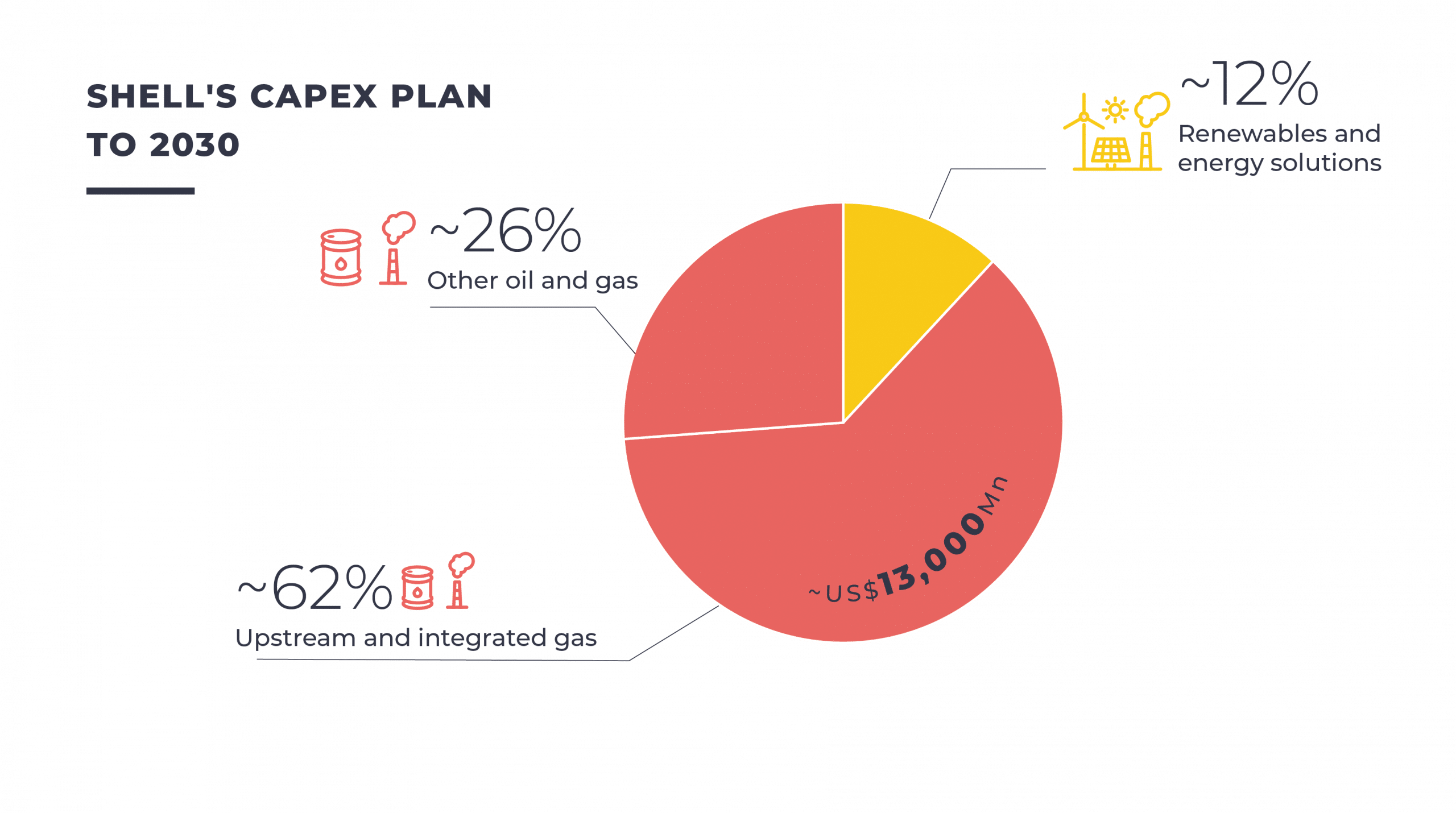

- Up to 2030, Shell plans to allocate approximately 62% of its investments to its “upstream and integrated gas” segment. Only around 12% will be earmarked for its “Renewables and energy solutions” business. This is a rollback compared to Shell’s previous capital expenditure plan, which targeted 19% of its 2025 investments in “Renewables and energy solutions” activities.

Shell’s fossil fuel production plan

Shell has made no commitment to stop developing new oil and gas projects. The company is the 12th largest upstream developer worldwide and the 4th largest LNG export terminal developer.

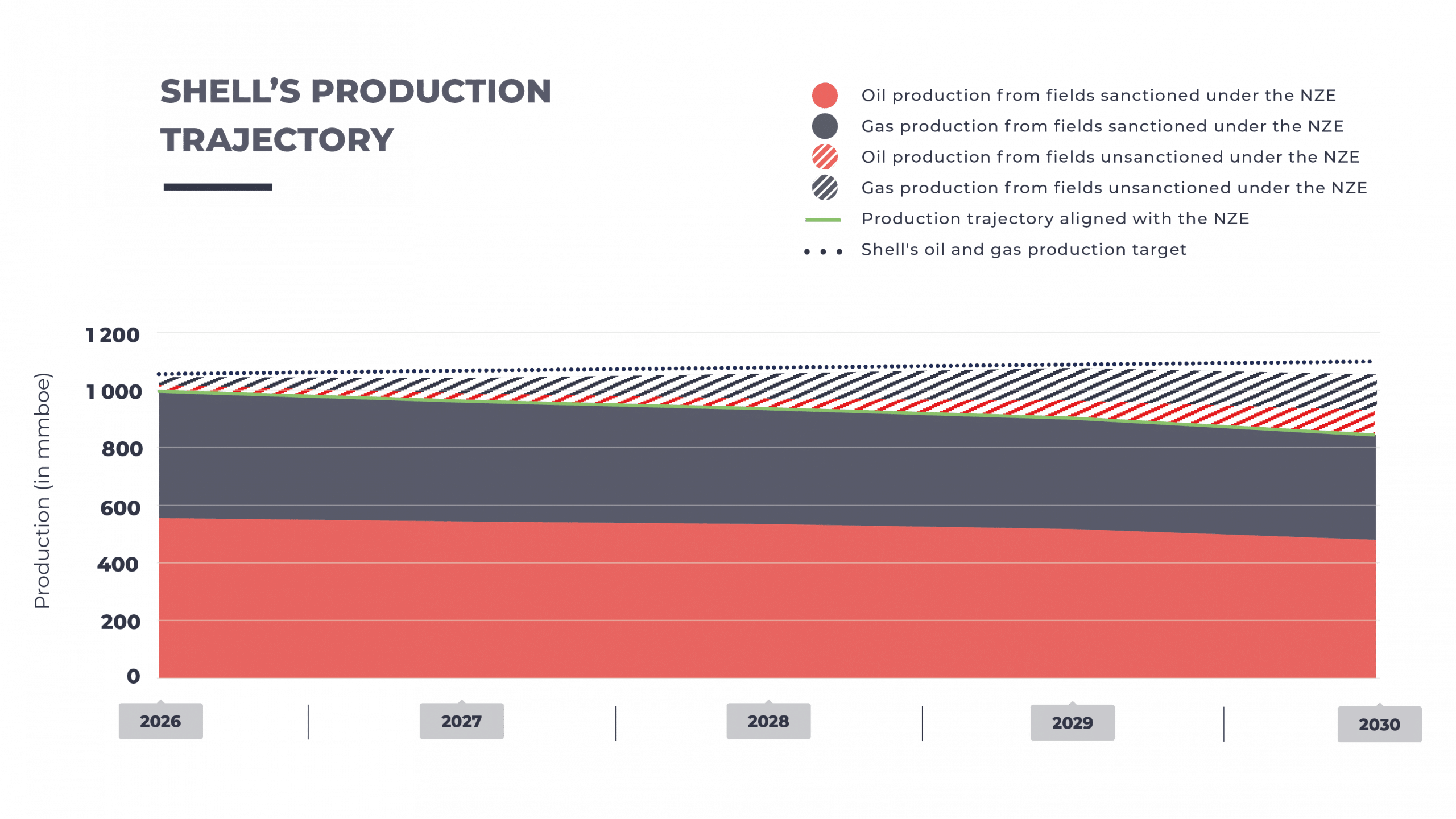

In 2023, Shell had already reviewed its oil production reduction target in 2030. In 2025, the company committed to increase its oil and gas production by 1% per year by 2030, driven by gas. With the company’s current expansion strategy, its 2030 fossil fuels production will be 23% above the NZE.

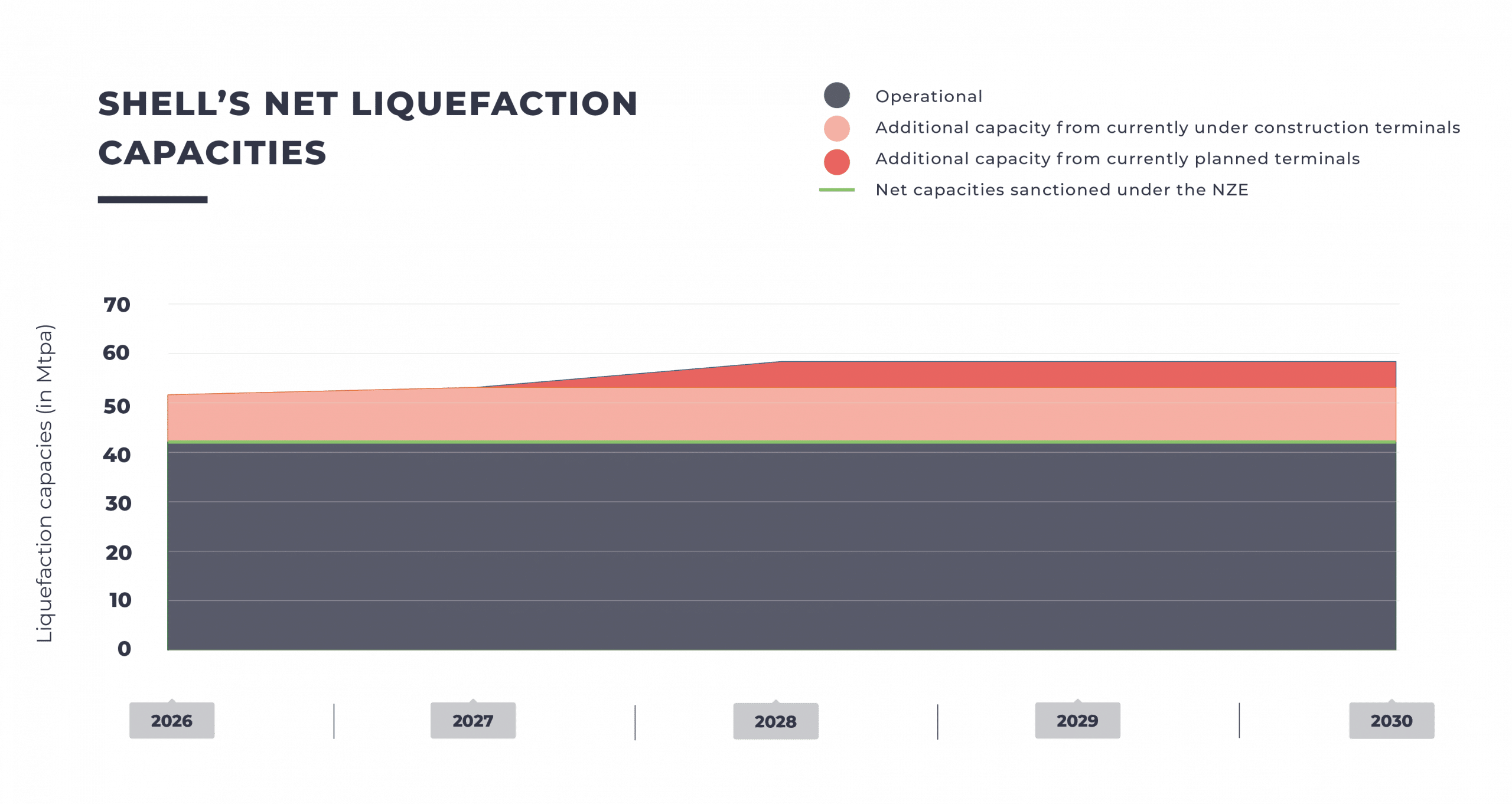

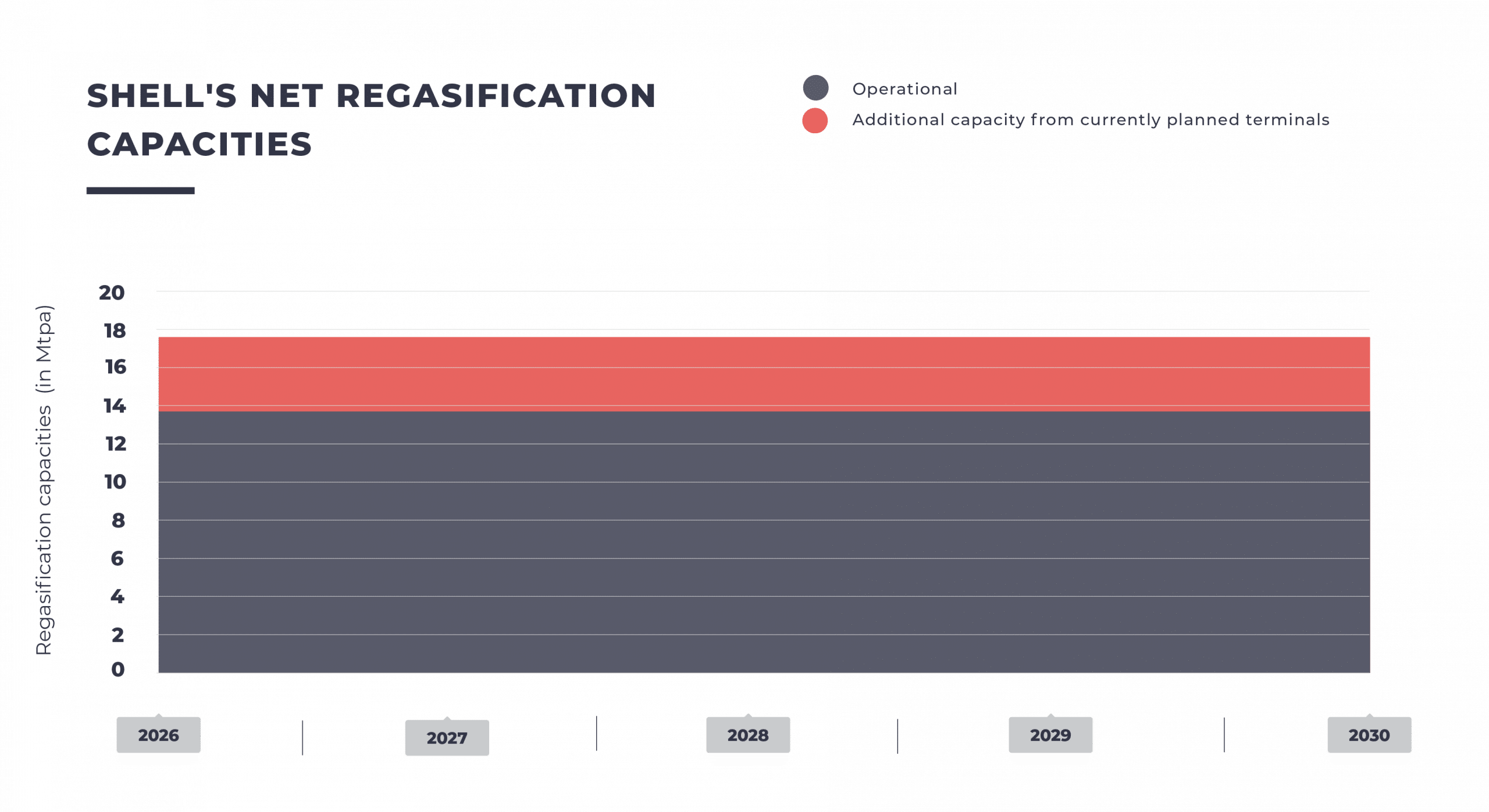

LNG is core to Shell’s fossil expansion strategy with new export and import terminals planned. Shell’s net liquefaction capacity will increase to 58 Mtpa by 2030 and will overshoot by 39% the level required by the NZE.

Shell’s diversification strategy

The company’s business model will continue to be based on oil and gas extraction and LNG in the coming years. Diversification in other energies will keep representing a minority share of its future production and will sometimes involve activities that are harmful to the environment.

A central part of Shell’s power strategy relies on gas power. Shell is planning 3 new gas power units that will represent a 12% increase of Shell’s gross gas power capacity.

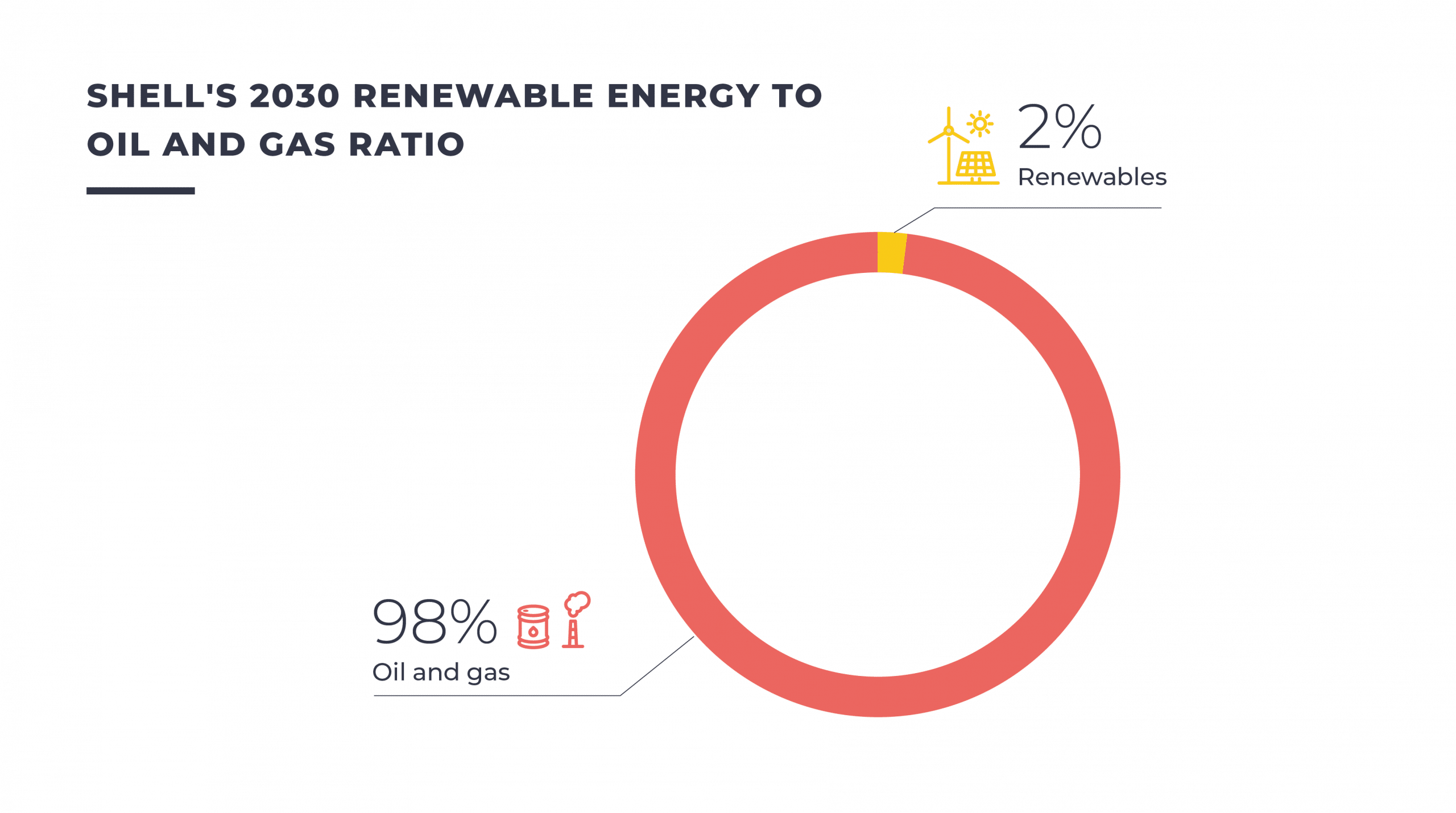

Shell does not communicate a target on its future renewable capacities. Its current installed and under development renewable portfolio capacity reaches 7.4 GW. Assuming these projects will be carried out by 2030, without any other portfolio change, Shell will still be producing 47 times more energy with its oil and gas extraction than with its renewable capacities in 2030.

With its current strategy, Shell will remain one of the key oil and gas players. Indeed, in 2030, Shell’s oil and gas extraction will represent 2.5% of the global hydrocarbon production projected in the NZE, whereas the company will only represent 0.1% of the worldwide renewable power production.

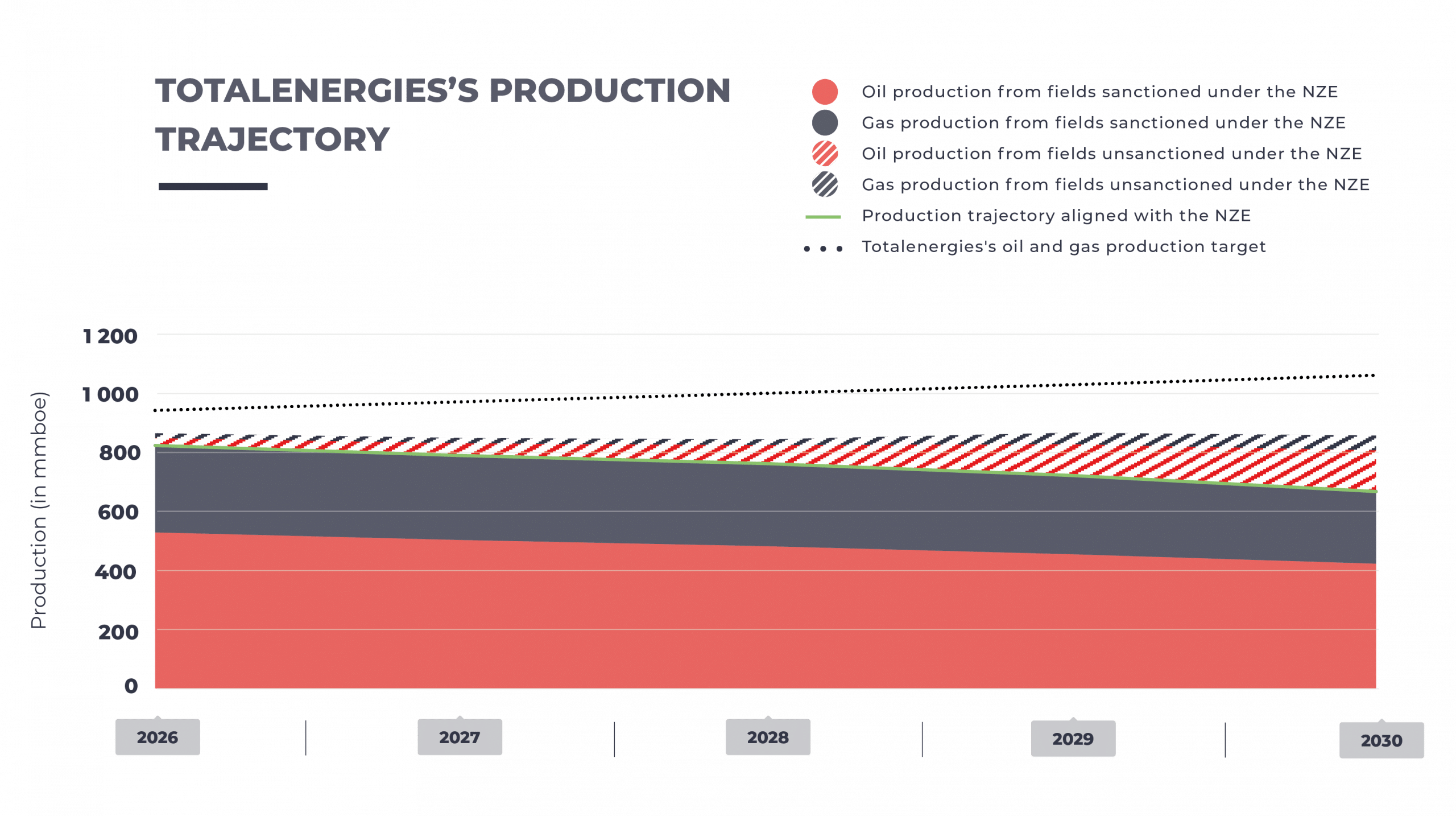

TotalEnergies’ investment strategy

The French company’s investment strategy heavily relies on hydrocarbons, in particular on upstream and LNG.

- From 2023 to 2025, TotalEnergies invested US$947 million per year in oil and gas exploration.

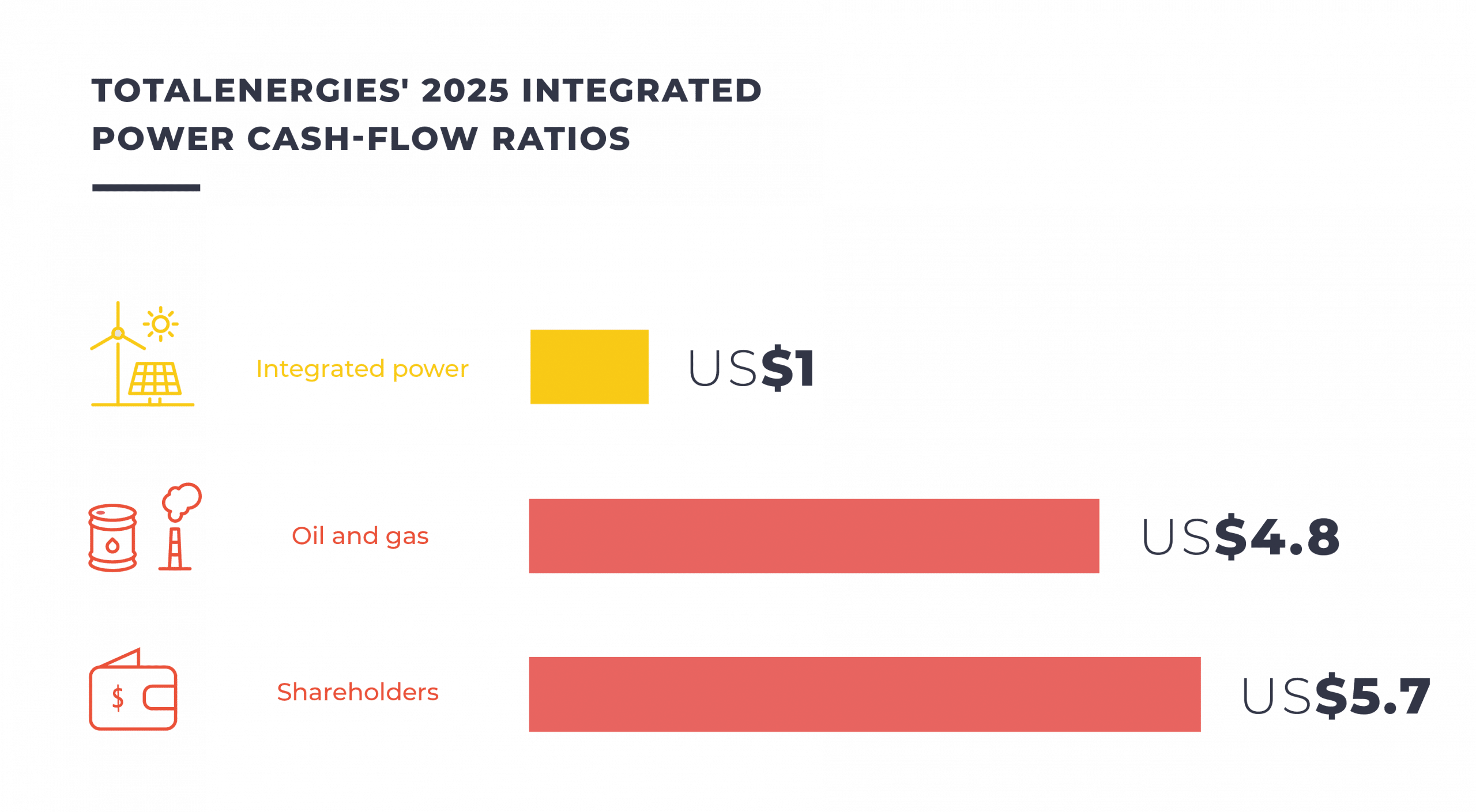

- In 2025, US$13.4 billion were invested by TotalEnergies in oil and gas – primarily upstream and LNG – and US$15.8 billion were distributed to shareholders, whereas only US$2.8 billion went to its “Integrated power” business – that includes renewable power and gas power.

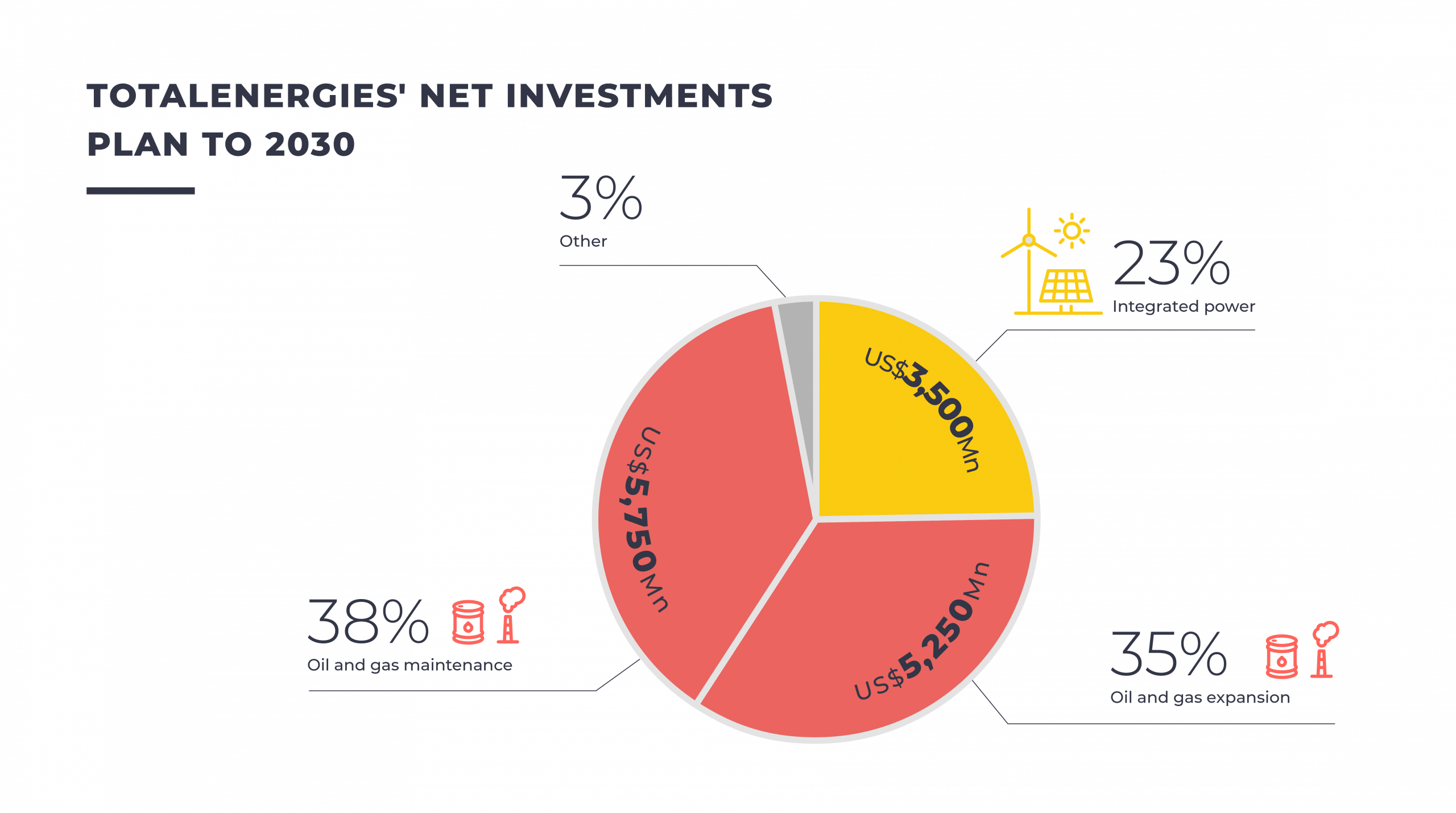

- Through 2030, TotalEnergies plans to allocate approximately 73% of its investments to oil and gas activities. Only 23% is earmarked for its “Integrated power” business, and around 3% for its “low carbon molecules” business. Also, a significant share of the amount going to “Integrated power” will correspond to the US$5 billion transaction between TotalEnergies and EPH, announced in November 2025. With this purchase, the French major confirms its gas-centered strategy, as gas power accounts for 81% of the purchased portfolio (along with biomass and BESS).

TotalEnergies’ fossil fuel production plan

TotalEnergies has made no commitment to stop developing new oil and gas projects. The company is the 6th largest upstream developer worldwide and the 12th largest LNG export terminal developer.

TotalEnergies came back on its oil and gas production target. While it was at some point forecasting a 2-3% annual growth in oil and gas production through 2028, the company now plans to increase it by 3% per year to 2030, with a growth exceeding 3% in 2025 and 2026. With the company’s current expansion strategy, its 2030 fossil fuels production will be at least 59% above the NZE.

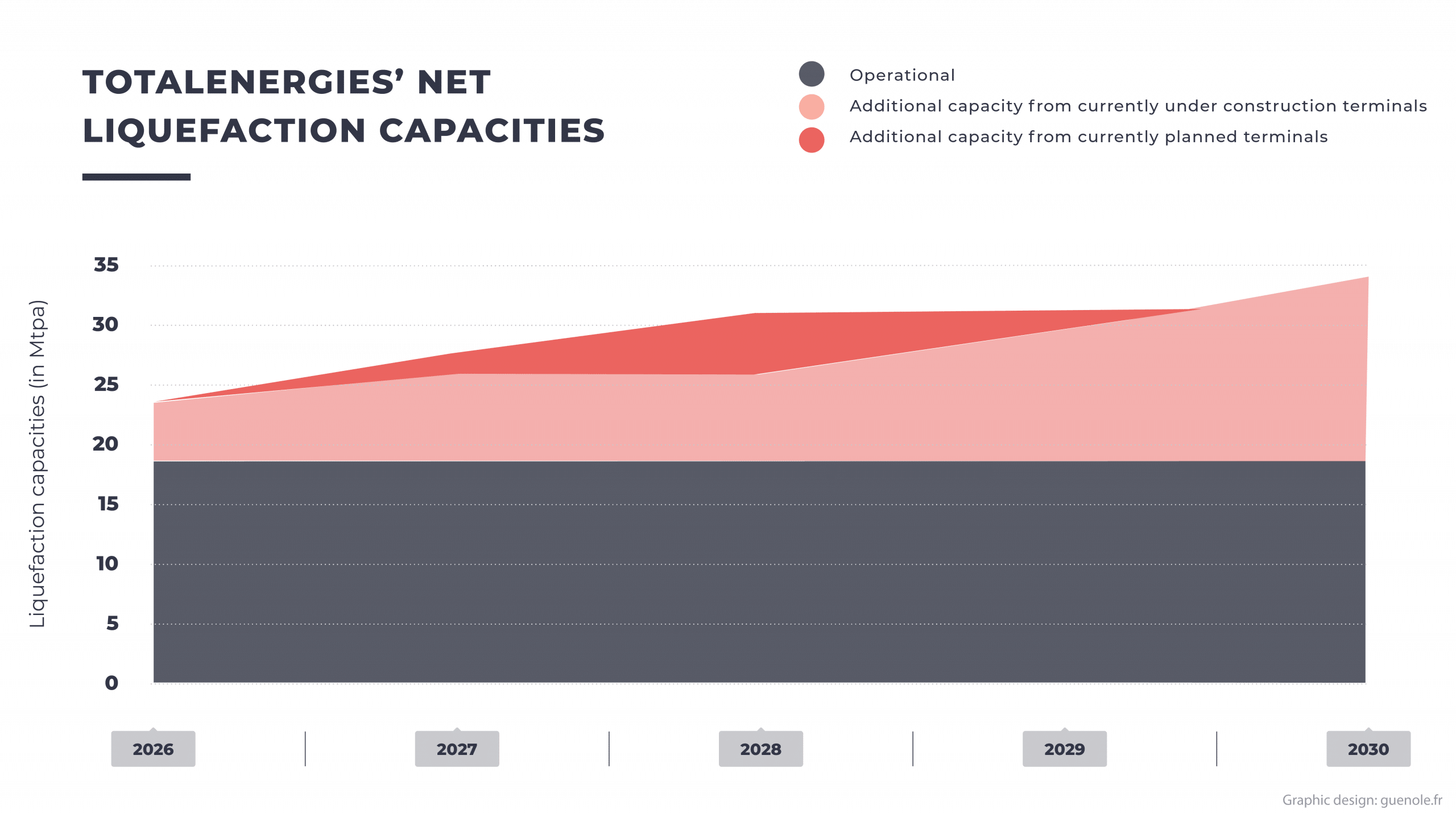

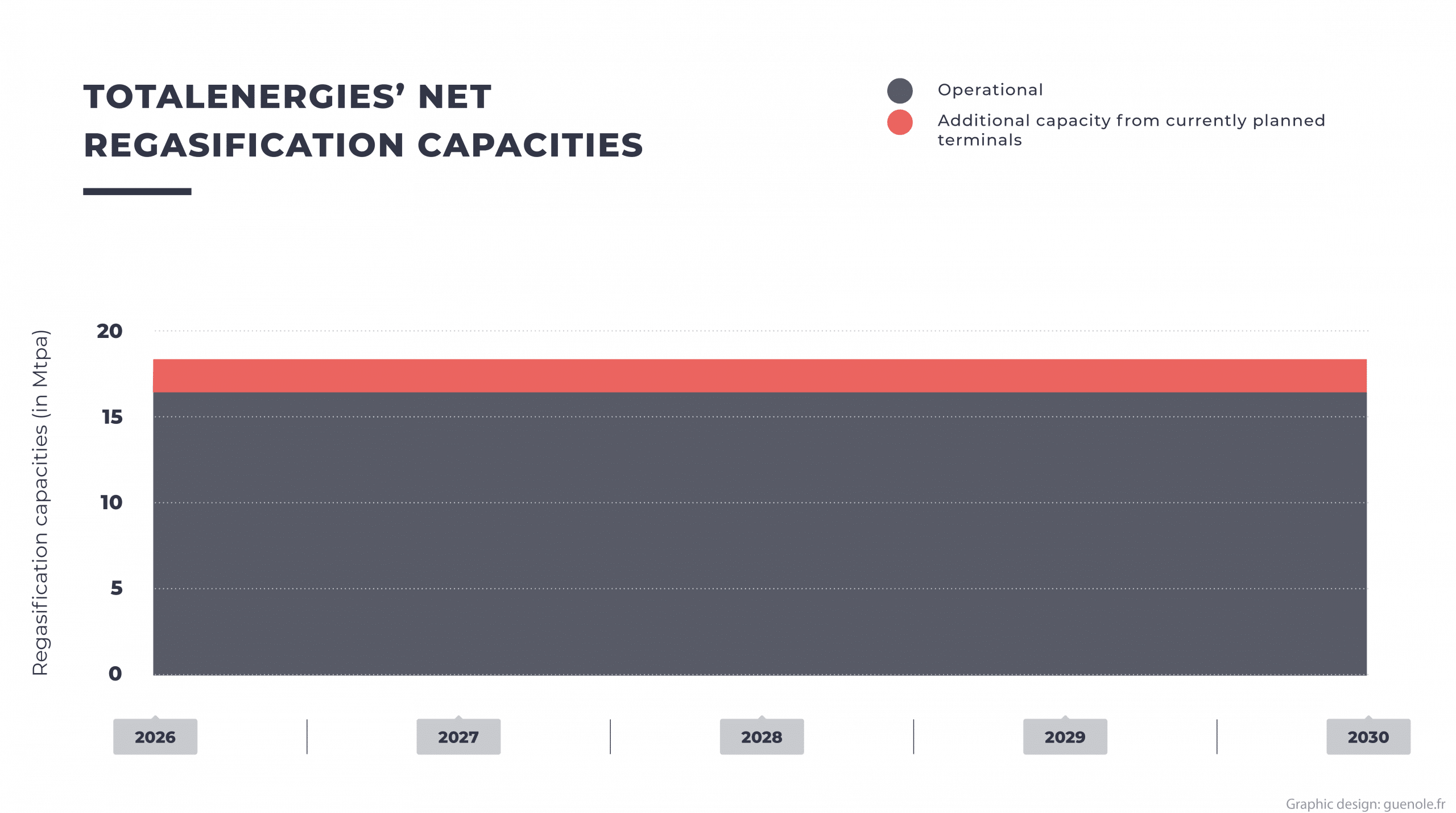

LNG is core to TotalEnergies’ fossil expansion strategy with new export and import terminals planned. The major’s net liquefaction capacity will increase to 36 Mtpa by 2030.

TotalEnergies’ diversification strategy

The company’s business model will continue to be based on oil and gas extraction and LNG in the coming years. Diversification in other energies will keep representing a minority share of its future production and will sometimes involve activities that are harmful to the environment.

A central part of TotalEnergies’ power strategy relies on gas power. TotalEnergies is planning six new gas power units and plans to double its gas power production by 2030. Gas power will then represent more than 30% of the company’s electricity production.

TotalEnergies plans to develop its renewable energy activities, with a capacity increase from 15 GW today to around 58 GW by 2030. Renewable power should then represent 8% of TotalEnergies’ production mix.

With its current strategy, TotalEnergies will remain one of the key oil and gas players. Indeed, in 2030, TotalEnergies’ oil and gas extraction will represent 2.3% of the global hydrocarbon production projected in the NZE, whereas the company will only represent 0.3% of the worldwide renewable power production.

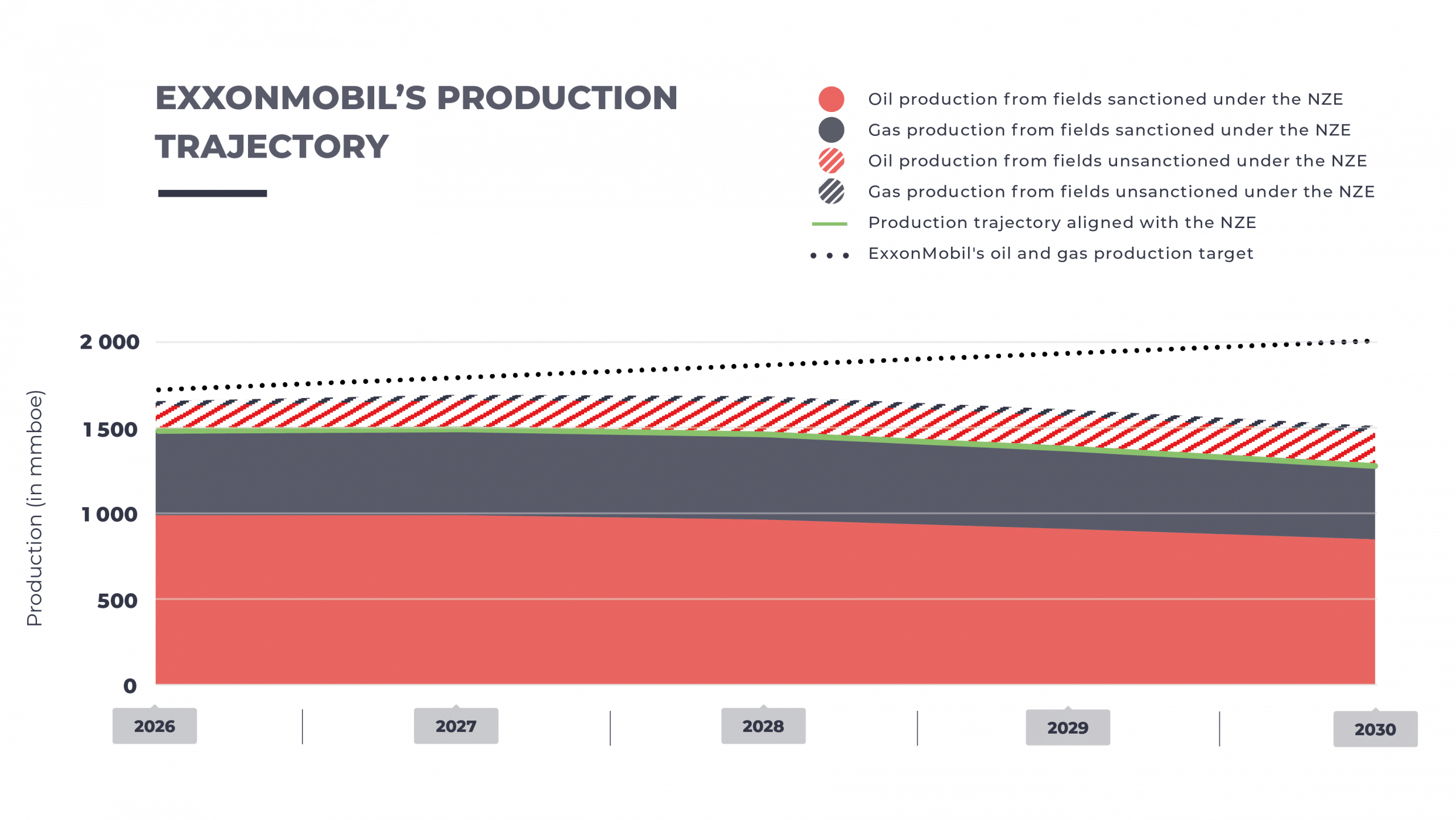

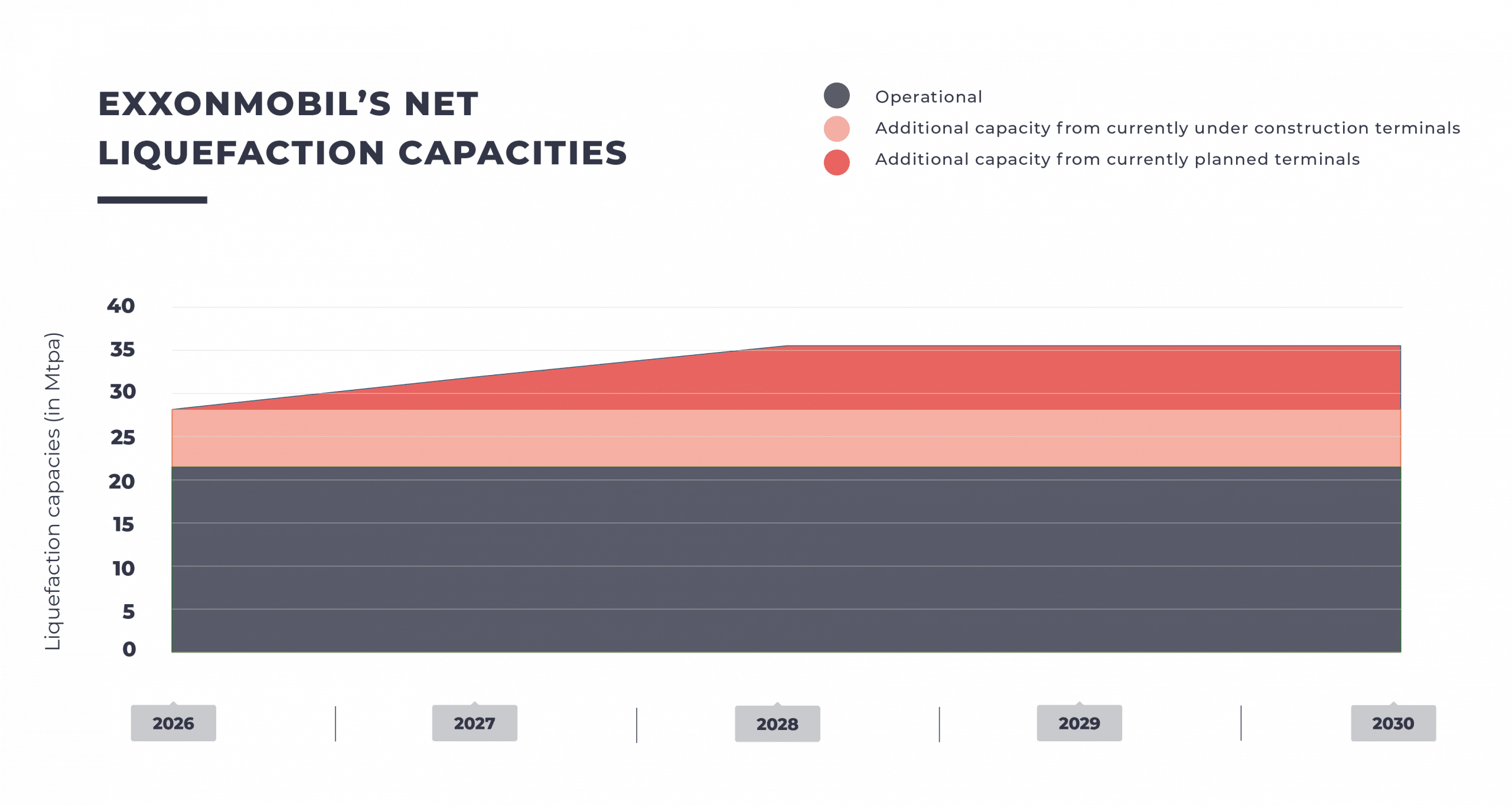

ExxonMobil’s investment strategy

- The US company’s investment strategy heavily relies on hydrocarbons, in particular on upstream and LNG.

- Between 2023 and 2025, ExxonMobil invested US$1.1 billion per year in oil and gas exploration.

- In 2024, US$28.4 billion were invested by ExxonMobil in oil and gas – primarily upstream – and US$37.6 billion were distributed to shareholders. ExxonMobil did not report any investment in renewable power for 2025.

- By 2030, ExxonMobil plans to invest approximately US$29.8 billion per year, of which US$3.3 billion should go to “low-carbon solutions”. This term includes CCS, hydrogen, biofuels or carbon materials, but ExxonMobil does not plan to invest in renewable power generation.

ExxonMobil’s fossil fuel production plan

ExxonMobil has made no commitment to stop developing new oil and gas projects. The company is the 5th largest upstream developer worldwide and the 19th largest LNG export terminal developer.

In early 2025, ExxonMobil set a new oil and gas production target: the company said to be aiming at 5.4 million barrels of oil equivalent per day by 2030, a major increase compared to the previous provision (4.2). At the end of 2025, ExxonMobil further extended this objective to 5.5 million barrels of oil equivalent. With the company’s current expansion strategy, its 2030 fossil fuels production will be 53% above the NZE.

LNG is central to ExxonMobil’s fossil expansion strategy with new export and import terminals planned. The major’s net liquefaction capacity will increase to 36 Mtpa by 2030 and will overshoot by 65% the level previously required by the NZE.

ExxonMobil’s diversification strategy

The company’s business model will continue to be based on oil and gas extraction and LNG in the coming years. Reported diversification in renewable power is non-existent.

Diversification in other energies will keep representing a minority share of its future production and will sometimes involve activities that are harmful to the environment.

A central part of ExxonMobil’s power strategy relies on gas power. ExxonMobil is planning six new gas power units, that will represent a 68% increase of its gross gas power capacity.

With its current strategy, ExxonMobil will remain one of the key oil and gas players. Indeed, in 2030, ExxonMobil’s oil and gas extraction will represent 4.4% of the global hydrocarbon production projected in the NZE.