UBS AM, the asset management arm of the Swiss group UBS and one of the top 20 global asset managers with $1.1 trillion invested assets, published in March 2021 its first exclusion policy related to thermal coal. While an exclusion threshold is included for the mining sector, nothing is done for the coal power sector. UBS AM also continues to support companies developing new coal mines or new coal plants. In addition, UBS AM does not mention any strategy for a global coal phase-out by 2030 in European and OECD countries, and 2040 worldwide. This is clearly a missed opportunity.

1. What’s new

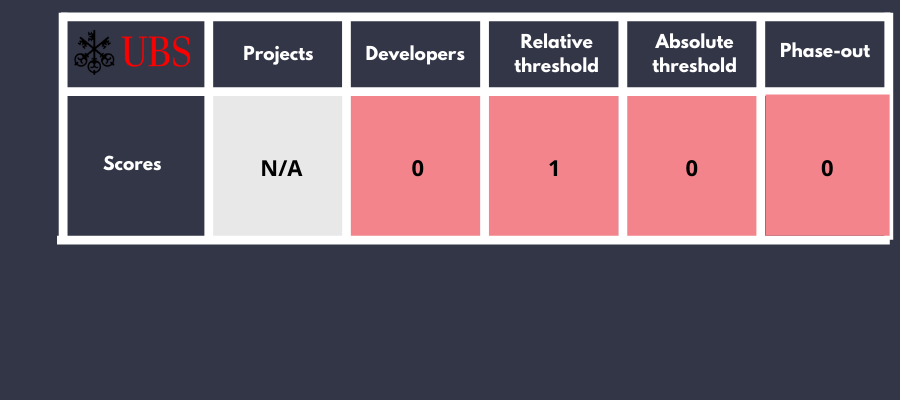

The core of UBS AM’s new coal policy lies in one line: it does not invest in companies that generate 30% or more of their revenues from thermal coal mining (including lignite, bituminous, anthracite and steam coal) and its sale to external parties.

These exclusions apply to active fixed income and equities funds under the direct management of UBS AM. Investments in other funds (including ETFs and single investor funds / mandates) and derivatives on indices are excluded from this rule. Derivatives on single names, a type of derivative where there is only one reference entity, are included in this exclusion rule.

2. Our analysis: only the beginning

With this first coal policy, UBS AM is finally realizing the need to implement an exclusion policy and we welcome this first step forward. But UBS AM’s commitments are extremely limited and only cover a reduced part of the coal industry. The scope of implementation is also limited. Therefore, this policy will not be sufficient to significantly reduce UBS AM’s support to the coal sector. According to recent financial research, UBS AM owned shares and bonds of 167 coal companies listed in the Global Coal Exit List in the sum of $3.9bn and $1.2bn respectively as of November 2020.

Despite the adoption of its first coal policy, UBS AM could still invest in 648 companies of the GCEL, while excluding just 287 of them.

The giant loophole in the policy is that UBS AM totally omits to consider coal power companies, while several of its global peers also apply exclusion such as Amundi, AXA IM or Ostrum AM. According to research by Climate Analytics based on the latest IPCC report, all coal plants must be closed by 2030 in OECD and European countries and by 2040 worldwide. This is why the Swiss asset manager should adopt a coal phase-out strategy by the same deadlines, covering coal mining as well.

At the same time, even if UBS AM adopts a 30% exclusion threshold for coal mines companies, the Swiss Asset Manager can still support 58 coal mining companies below the 30% threshold such as Glencore (about 20% of coal revenues but 123Mt of coal extracted annually, $97m investments). This is why to consider the real impact on climate and health of coal companies, UBS AM should complement its relative exclusion criterion with an absolute one and immediately exclude companies that produce more than 10 Mt of coal per year and commit to lowering these thresholds to zero.

UBS AM is also turning a blind eye to coal developers planning new coal mines, plants or infrastructure projects, even though more than 1,000 new coal power units are being planned, increasing the coal capacity by nearly 40%. UBS AM will thus be able to continue to support the mining company Adani (below 30% of revenues from thermal coal mining, $8m invested) although the Indian Group plans to build new coal mines in Australia and India and to add 3.3GW to its coal power capacity. UBS AM must immediately recognize the global consensus on the need to end the expansion of the coal sector now, and exclude all coal developers, without exception, such as Amundi.

Moreover, the scope of implementation of this policy is relatively limited for several reasons:

- Our own research and exchanges with UBS AM allow us to assess that only 36% of Assets under Management (AuM) are covered by this coal exclusion policy.

- The share of the UBS AM’s passively managed assets represents about 42% of total AuM and these assets are not covered by this exclusion policy.

- UBS does not specify its strategy for new mandates. Will this exclusion policy be offered by default to clients (opt-out option)?

UBS AM’s Scores in the Coal Policy Tool

This table presents the coal scores of UBS AM based on five criteria of the Coal Policy Tool

3. Our conclusion

Comparing the first UBS AM coal policy to that of the UBS Group allows us to reach two conclusions: firstly, there is a lack of consistency, with the asset manager excluding mining companies while its mother company also excludes power companies; secondly, both financial players are still very far from a robust coal policy.

UBS AM must urgently react to align with the best practices in the sector from Amundi, AXA IM or Ostrum AM, starting with the exclusion of all coal developers and the coverage of the coal power sector. The Swiss asset manager must also review the scope of its policy, which is currently far too limited. In addition, UBS AM should detail an overall strategy to fully exit coal at the latest by 2030 in EU and OECD countries, and 2040 worldwide. The asset manager should finally also start to tackle oil & gas now to face the climate emergency.