Maybank, the first banking group in Malaysia with US$165 billion in assets, has announced, at its annual general meeting in May 2021, its first measures to exclude part of the coal sector from its financing activities. However, its commitments are extremely limited. They do not even match the earlier commitments of CIMB, its national competitor. Maybank must seize the opportunity of the publication of its upcoming “coal value chain framework” to significantly strengthen its coal exclusion criteria.

1. What’s new

Maybank’s first coal policy announcement mentions the commitment of “no financing of new coal activities”. In its 2020 Sustainability Report, Maybank is more precise and commits to not financing “any new coal mining activity” while applying a stringent “ESG risk impact assessments” for coal plant financing. It also mentions the development of a ‘coal value chain framework” covering both the coal mining and coal power sectors.

2. Our analysis: a very timid first coal policy

Maybank is a sizeable regional bank, among the top 5 banks in South East Asia, which financed several coal projects recently such as Java 9 and 10 in Indonesia or Nghi Son 2 in Vietnam, as well as coal companies in the ASEAN region. It has channelled at least US$1.7 billion to the coal sector between October 2018 and October 2020, through loans and underwriting deals to 6 large coal companies that currently operate 30.7 GW of coal power, almost the equivalent of Indonesia’s total coal power installed capacity.

If the decision by Maybank to adopt its first coal exclusion policy is welcome, it is extremely disappointing to see its severe limitations: it is highly insufficient in its contribution to the climate goals of the Paris Agreement. From the policy elements provided, it seems to focus exclusively on dedicated project financing and not on general corporate financing activities, and to exclude specifically new coal mines deals but not new coal plants ones. We have contacted Maybank and are waiting for their answers to clarify several points.

If confirmed, these limitations mean Maybank’s policy is not even as ambitious as CIMB or DBS coal policies, both of which end direct financing to new coal plants, with DBS also curbing its support towards certain coal developers. Considering the coal companies Maybank supported recently are collectively planning 13.2 GW of additional coal power capacity, this must clearly be the next step for the bank: ending all support to coal expansion.

If Maybank must also stop financing highly exposed companies in the coal sector by implementing strict exclusion thresholds for coal mining and coal power companies (maximum 20% of revenues or of coal share of power production & maximum 5 GW of coal plants or 10Mt of coal extracted), another key and more urgent gap in its policy is the absence of a coal phase-out commitment. The Malaysian bank must follow climate science and exit the coal sector by 2040.

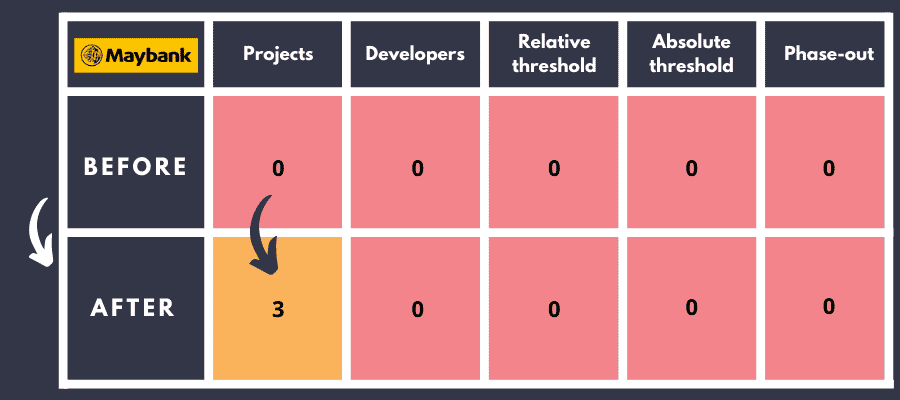

Maybank’s Scores in the Coal Policy Tool

3. Conclusion

Whilst having a coal policy is better than not having one, Maybank commitments are clearly lagging behind many of its peers, and do not meet the minimum standard of the end of the direct financing of new coal plants. When drafting its future “coal value chain framework” Maybank must fill this gap and immediately stop the financing of all coal developers, the minimum for a bank that claims to work for a “climate-resilient society”.

Maybank also needs to catch up on its peers by committing to strong steps to become completely fossil free, for instance copying the ambitious 2045 total fossil fuel phase-out commitment adopted by Nedbank (South Africa) earlier this month.