Bank of Montreal (BMO) is a sizeable international bank (US$ 665 billion in assets) based in Canada. It announced its new coal policy on the 10th of March 2021. The result is very disappointing with an overall policy that will have almost no impact on BMO’s banking practices. The Canadian bank copied the bad coal policy adopted by RBC, with all its loopholes, instead of following the lead of Desjardins, which adopted a robust coal policy last December.

1. What’s new

In March 2021 BMO adopted its first coal policy for its banking activities that encompasses the following elements:

- BMO will stop financing, as a lender, new greenfield thermal coal mines and new greenfield coal plants or the significant expansion of existing projects;

- BMO will implement a 60% maximum threshold of coal revenues or of coal share of power production for new clients, and stop financing existing customers over this threshold except “if the client can provide satisfactory evidence that they are reducing or have defined plans to reduce their use of thermal coal”.

2. Our analysis – BMO’s coal policy has no bite

BMO is currently deeply involved in coal financing with $5.3 billion in 25 coal companies. This means very concretely that it supports companies collectively extracting 348Mt of coal annually, with a combined coal power capacity of 85.7 GW. This is the equivalent of the operating coal power capacities of Canada, the UK, Brazil, Mexico, South Korea and Australia combined.

In light of this involvement, BMO first coal policy is, unfortunately, very weak.

Firstly, BMO does not end the direct financing of all new coal projects, whereas it would have been easy for the bank to do so since the records show no such project financing since 2002. If the policy seems to cover both coal mining and coal power projects, it nevertheless incorporates a key loophole: it only fully covers greenfield projects, which is very problematic because brownfield projects must be stopped too.

BMO must therefore stop financing all new coal mining and coal power projects, without exception, and exclude all companies involved in the development of new coal projects.

Regarding its decision to implement a maximum 60% threshold of coal revenues or of coal share of power production, this is very disappointing for two reasons:

- This threshold is far too high and very rare – almost unprecedented – in the sector, since most banks use a 50% or 30% exclusion threshold – best practices recommend 20% or less;

- Worse, BMO will apply such threshold only to new clients and plans on allowing exceptions for new clients if they can present loosely defined “satisfactory evidences” of their willingness to reduce their coal exposure.

In other words, to avoid having a meaningless policy, BMO must erase these two exceptions and go much further by reducing drastically such threshold: if it was to apply it strictly to its current customer this would only mean divestment of 6% of its current coal exposure (Center Point, Gulf Power, PPL, TransAlta & Peabody).

Last but not least, by not committing to any binding comprehensive coal phase-out strategy, BMO lacks an essential component of any proper coal policy. We therefore call on BMO to follow the example of Desjardins Group, the first Canadian financial player which adopted a robust coal policy last December.

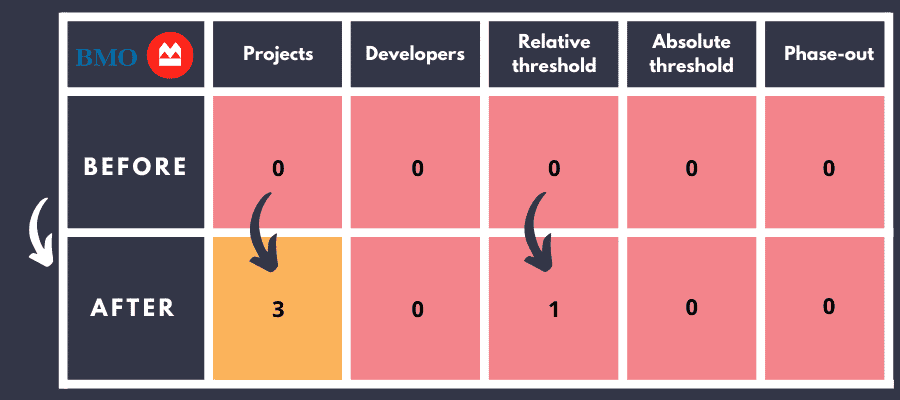

BMO’s Scores in the Coal Policy Tool

Conclusion

With the weakness of its exclusion criteria and all the loopholes identified, this new coal policy seems like a non-policy and will have almost no impact on BMO’s activities. It is extremely disappointing to see BMO’s announcement translate into such toothless policy.

BMO must quickly go back to the drawing board and produce an improved and meaningful coal policy, before then starting working on all the other fossil subsectors to cover the oil & gas industry as well.