Generali is a major insurer worldwide – the largest in Italy, and in the top 10 worldwide – with €70.7 billion of premiums written and €500 billions of assets under management. On the 30th June 2021, it published a new technical note on climate change, updating its fossil fuel exclusion policy.

The adoption of a Paris-aligned coal phase-out commitment for its underwriting and investment activities worldwide, including in eastern Europe, must be praised. Similarly the tightening of coal exclusion criteria for its asset owner activites is welcome. Some gaps remain including the absence of exclusion for coal companies for its underwriting activities, and risks for potential exceptions are high. The absence of any policy for its asset management branch, Generali Investments, is also noticeable. Finally, while Generali sets a first standard on oil and gas, it could have been more aggresive considering its limited exposure to these sectors. In other words, if Generali makes progress, certain gaps are yet to be filled.

1. What’s new

By updating its fossil policy, Generali is implementing the following new measures:

On coal:

For both its investments as an asset owner and underwriting activities, Generali has committed to reach zero exposure to thermal coal following a Paris-aligned timeline: 2030 for OECD countries, 2040 worldwide (2038 for its underwriting activities).

For its investment portfolio as an asset owner, Generali now implements the following exclusion criteria:

- all coal power developers (planning over 0.3 GW of new coal power capacity), whereas it was previously excluding only the 120 top coal plant developers of the Global Coal Exit List;

- companies for which more than 20% of revenues derive from coal or 20% of energy produced derive from coal, from 30% before;

- companies extracting over 10 million tons of coal annually, from 20 million tons before, or with over 5 GW of coal power capacity.

These criteria apply for both new and existing clients, but for the latter with two exceptions: if the company has adopted a decarbonization or coal phase out strategy aligned with a 1.5°C trajectory, unless it is developing new coal capacities, or if the company is located in a country highly dependent on coal power production (over 45% of the national power mix).

On oil & gas:

There is no change on the investment side: Generali retains an exclusion on tar sands for companies with over 5% of tar sands, or involved in the building of controversial pipelines. However, for its insurance coverage, Generali has now extended its commitment from tar sands to all upstream oil & gas underwriting (with an exception for companies’ insurance packages where below 10% of coverages offered are linked to oil & gas assets). It also specifically exclude all insurance to shale oil & gas and Arctic oil & gas assets: it will not underwrite risks associated with exploration, production and related pipelines for shale oil & gas, and exploration and production of oil and gas in the Arctic, both onshore and offshore.

2. Our analysis: heading in the right direction, but important gaps remain

On coal: a Paris-aligned end goal, but missing steps to reach it

Regarding its coal investments, Generali makes some important progress: for its investment activities as an asset owner, it now bans all the 256 coal plant developers indicated in the Global Coal Exit List (GCEL). The adoption of a coal phase out strategy is also an unquestionable step forward. By applying much stricter coal exclusion criteria that are aligned with international best practices (maximum 20% revenues or coal share of power generation, 10 million tons of coal extracted annually and 5 GW of coal power capacity), and a commitment to lower them to a full exit from the sector on a timeline aligned with climate science, Generali seems to be almost there.

However, by not covering coal mines and coal infrastructure developers, this still leaves out of the scope of this exclusion policy 79 companies still active in the expansion of coal worldwide, according to the GCEL.

However, several elements question the effective ambition of such commitments.

First, its exemption framework creates gaps in its coal exclusion criteria for its investments as an asset owner whereas Generali’s exposure was already limited (227 million invested in 54 companies). This is problematic on the extent its exposure was mostly centred on eastern European countries. By adding an exception specifically for such countries (highly dependent on coal electricity), its policy becomes less coherent. This might mean that Generali could continue to invest in PGE in Poland or CEZ in Czech Republic in spite of their high coal involvement. The second exception for companies whose transition plans or strategy is deemed aligned to a 1.5°C trajectory further weaken its exclusion policy.

Then, regarding its underwriting activities, while Generali recently said it will no longer insure 4 companies involved in coal activities including CEZ in Czech Republic from 1st January 2022, the room is still open for insurance coverage to be offered to companies highly active in the coal sector, including coal developers. Indeed, Generali fails to implement exclusion measure to its underwriting activities that target companies as a whole but only forbids exposure to coal assets of new clients. This maintains a double standard between its underwriting and investment activities.

Last but not least, this updated coal policy still does not cover Generali’s asset management activities whereas most of the assets under management of Generali Investments are the assets of Generali itself. This is another gap in the Group’s coal policy that leaves out an important branch of Generali, whereas extending its investment commitments to the assets managed for other institutional investors by Generali Investments could have been done at little cost.

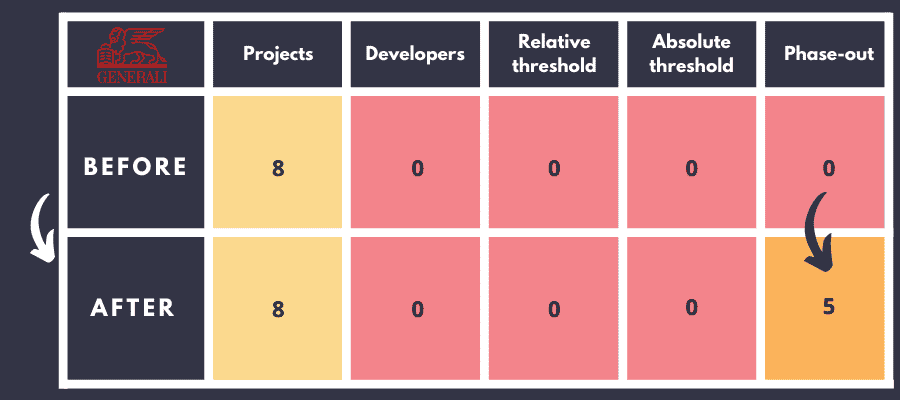

The scores of Generali (insurer) in the Coal Policy Tool

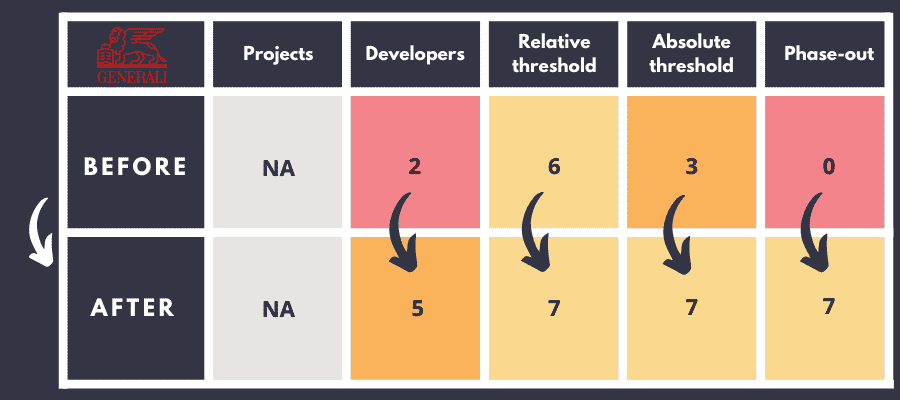

The scores of Generali (asset owner) in the Coal Policy Tool

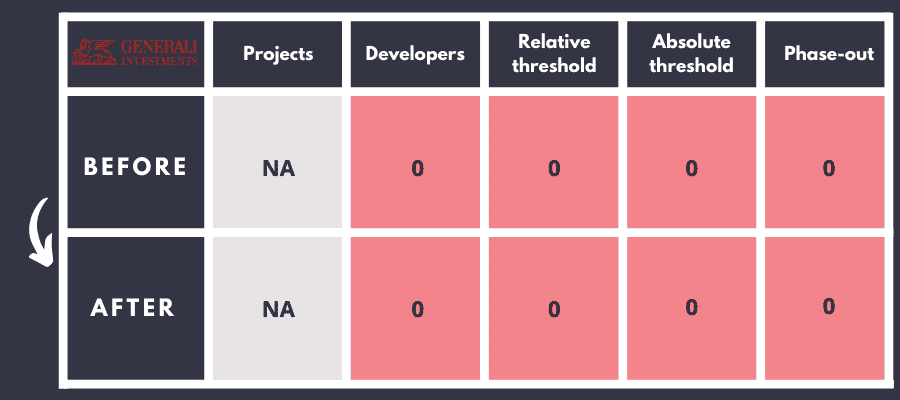

The scores of Generali Investment (asset manager) in the Coal Policy Tool

according to the five criteria set out in the Coal Policy Tool

On oil & gas: limited commitments, considering the starting point

Taken aside the investment activities, where no new announcement is made by Generali, the new oil & gas commitments regarding its underwriting activities are a positive development putting it in top of the pack regarding oil & gas insurance, even if more is needed to align with the objectives of the Paris Agreement. The new commitment intelligently targets oil & gas upstream assets by ending stand-alone insurance coverage to such assets, and by strongly limiting these coverage for insurances offered to companies as a whole.

However, Generali should now commit to stop supporting all oil & gas expansion projects in both conventional and unconventional sectors, and to commit to an ambitious oil & gas phase out date that implies the oil & gas companies it still insures adopt their own oil & gas transition plan. For instance, Suncorp Insurance has already committed to end all oil & gas coverages in its portfolio by 2025 for the latest. At a moment when even the IEA says no new fossil fuel projects must be financed to be on a net-zero by 2050 track Generali therefore needs to go further on oil & gas, starting by withdrawing its support to expansion in the sector.

Conclusion

The new exclusions adopted by Generali mark a stark improvement regarding the logic of its long-term strategy to reach zero coal exposure in its investment activities. The adoption of a coal phase out deadline for its underwriting activities is also welcome. However, when it comes to immediate exclusions, the announcement could have been more ambitious considering certain important gaps remain. The fact Generali does not commit to end all financial support towards coal developers is one of them. As a next step, it should apply the same policies as Allianz and Axa, which exclude all coal developers, or at least apply their asset owner policy to their insurance activities. Generali must also rapidly adopt its fossil fuel policy for its asset management branch, Generali Investments, that still does not have any coal policy more than five years after the Paris agreement.

The assessment is fairly similar for oil & gas. Generali could have been more ambitious than ending insurance coverage for most oil & gas assets in the upstream sector: insurance coverage to oil & gas developing companies must stop. Its exclusion criteria for its investment activities must also be aligned to the stricter criteria set for the insurance branch of Generali.