WEO 2021: the three principles for financial institutions

WEO 2021: the three principles for financial institutions

The World Energy Outlook (WEO) 2021 was intended to be the International Energy Agency’s (IEA) “guidebook” to COP26. Published just weeks before the global climate summit, it centered the IEA’s “Net Zero by 2050” (NZE) scenario and highlighted the gaps between this 1.5°C trajectory and the current international and national pledges and policies. Indoing so, the IEA set the new normal for the energy sector: a swift shift from fossil fuels to renewable energies, with an immediate end to new fossil fuel supply projects and a power system that swiftly reaches carbon neutrality. Here, Reclaim Finance analyzes the WEO 2021 and derives three principles that any financial institution that wish to reach carbon neutrality or align with a 1.5°C trajectory should follow.

States, companies and financial institutions have long used the IEA’s scenarios to build their energy strategies and investment decisions. In recent years, major financial players – like JP Morgan Chase, BNP Paribas or ING – have used the IEA’s Sustainable Development Scenario (SDS) to claim that they were aligning with the Paris Agreement and engage with energy companies. If these institutions were genuine in their desire to limit global warming and/or meet their own carbon neutrality pledges, they must now turn to the NZE that has been described by the IEA as the normative scenario in its WEO 2021.

Three main principles can be derived from the analysis of the WEO 2021 for any financial institutions that commit to align with a 1.5°C trajectory.

Immediately rule out support to fossil fuel supply projects, LNG and unabated fossil fuel power plants and the companies that develop them (see 1.a in the report).

According to the IEA, “no new oil and natural gas fields are required beyond those that have already been approved for development” in a 1.5°C trajectory. This means that all projects that have not reached a “final investment decision” by the end of 2021 are not compatible with limiting global warming to 1.5°C and thus financial institutions should not support such projects or – because much of the necessary fund come from corporate funding – the companies that develop them.

Similarly, the IEA underlines that most of the liquefied natural gas (LNG) projects already planned are “not necessary”. Following current industry plans, the LNG liquefaction capacity would be twice the demand by 2030 and most of the LNG projects would “not recover their invested capital”, resulting in $75 billion in stranded capital. LNG is also a major source of GHG emissions with a GHG footprint twice as big as that produced by the combustion of fossil gas, making development plans especially incompatible with climate targets.

As the NZE requires the power sector to reach carbon neutrality as soon as 2035 in “advanced economies” and by 2040 worldwide, new “unabated” fossil fuel power plants should not be supported. The IEA notably underlines that no new unabated coal power plants must be approved, and that unabated coal must be phased out altogether by 2040. Gas power generation also declines: gas electricity production is less than a third of 2020’s levels in 2040, with unabated gas falling by 90%. Furthermore, considering the high cost of CCUS, the current failures to develop CCUS plants and the overall uncertainties around CCUS deployment, abated gas plant development is likely to remain lower than the IEA’s expectations.

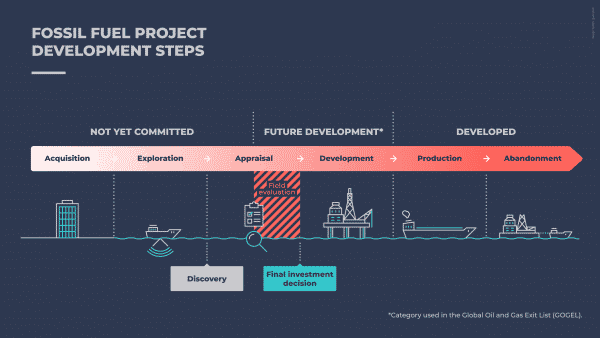

Using the Global Oil and Gas Exit List

The Global Oil and Gas Exit List (GOGEL) identifies companies that are developing new fossil fuel projects. The list features a “future development” category based on projects that have entered the development phase – after the final investment decision – or are in field evaluation – just before the final investment decision. Projects that are in field evaluation already require significant investments and are likely to reach a final investment decision. Therefore, the GOGEL can be used to identify which companies do not comply with the NZE.

Ensure the fossil fuel companies they support swiftly and drastically reduce their fossil fuel production and methane emissions (see 1.b, 2.a and 2.b in the report).

The NZE allows for substantially more coal and gas use than the 2021 UN Production Gap Report in the short term (see 2.a). In the NZE, coal supply declines by 56.7%, gas supply by 7% and oil supply by 19.8% from 2020 to 2030. The Production Gap report requires coal supply to be 31% lower and gas supply 21% lower than in the NZE in 2030. If gas supply drops by 42.3% from 2030 to 2040 in the NZE, the NZE fails to match the decline in gas outlined in other 1.5°C compatible pathways.

However, despite these shortcomings, the NZE still requires a drastic change in fossil fuel production plans for coal, oil and gas. For fossil fuel companies, merely aligning with the NZE means immediately initiating a swift reduction of fossil fuel production, thus shifting from model based on the growth of their fossil-based business to one where fossil fuel production is progressively phased-out and replaced by renewable energies. Financial institutions must ensure that the fossil fuel companies they support follow this trend and stop supporting those that do not.

Furthermore, the IEA emphasizes the need to cut methane emissions by 75% by 2030, notably through putting in place methane abatement measures and reducing fossil fuel production. It is worth noting that unconventional fossil fuels disproportionately contribute to methane emissions, notably when they are extracted through fracking. Financial institutions should therefore also ensure that companies swiftly reduce unconventional oil and gas production and quickly abate their methane emissions.

Ensure the companies they support do not rely on unproven technologies and improbable large-scale negative emissions to build their climate plans and favor renewable energies instead (see 2.a, 3.a and 3.b in the report).

The NZE largely rely on carbon capture and storage and biomass, two choices that could derail it from a 1.5°C trajectory and have significant negative sustainability effects.

While identifying CCS deployment as one of the main technological challenges to be overcome, the IEA bets the house on large levels of CCS in the NZE to abate the remaining emissions of fossil fuels. 1665 MtCO2 are captured as soon as 2030, more than three times the level of the IPCC’s P2 pathway and more than 41 times current levels. Historically, CCS capacity only slightly increased from 2010 to 2021 and only a very small fraction of planned CCS capacity entered operation. Concretely, only 27 CCS facilities are operational today with 4 under construction, and several major CCS projects costing billions that have failed in the past few years. As the Climate Action 100+ acknowledges, the high cost of CCS makes it a very costly decarbonization option, especially compared to increasingly competitive renewable energies. Furthermore, carbon capture consumes significant amounts of energy, thus having an uncertain effect on overall emissions.

In the NZE, biomass becomes a major energy source by 2050, rising from 62 EJ in 2020 to 102 EJ in 2050, with more than half coming from forest and wood (55 EJ). This level of biomass used greatly exceeds the levels seen in IPCC P1 and P2 scenarios. It disregards the fact that biomass use for power generation can emit large quantities of CO2 and have other negative environmental impact. The total land area dedicated to bioenergy production therefore increases from 330 million hectares (Mha) in 2020 to 410 Mha in 2050, the size of India and Pakistan combined and more than a fourth of total available cropland.

These elements should drive financial institutions to adopt a precautionary approach to CCS and biomass, ensuring that companies do not rely on them to achieve their climate targets. Financial institutions should instead push companies to develop renewable energies and lower their own energy needs. Despite potentially overestimating the cost of renewable energy, the IEAitself writes that “low technology costs andthe availability of low-cost financing in manymarkets means that policy makers couldestablish enabling conditions in which up to60% of the additional generation of solarand wind in the NZE could be achieved at noadditional cost to consumers”.

While the IEA is yet to chart a fully sustainable and low risk pathway to achieve carbon neutrality and limit global warming to 1.5°C, its NZE allows states, companies and financial institutions to clearly establish what is not compatible these objectives. Reclaim Finance urges financial institutions to follow the three principles laid out above, thus taking advantage of the NZE to ensure their own operations are not at odds with a 1.5°C pathway. These principles should shape both the exclusion and engagement policies of financial institutions.